The U.S. Federal Reserve’s (Fed’s) June Federal Open Market Committee (FOMC) meeting marked an important policy moment under new Fed Chair Kevin Warsh. As widely expected, the FOMC, the policy setting arm of the Fed, held the target range for the federal funds rate steady at 3.50% to 3.75% on June 17. While the rate decision came as no surprise to financial markets, the more notable developments were the tone of the policy statement, the updated economic projections, and Chair Warsh’s initial signals about how he may lead the Fed.

A Shorter Policy Statement and Minimal Forward Guidance

The June policy statement was much shorter and simpler than statements over the last eight years. It included the rate decision and a brief assessment of the economic and inflation outlook but removed much of the forward guidance markets had long become accustomed to.

In his post-meeting press conference, Chair Warsh indicated that the Committee had discussed forward guidance and concluded that it may no longer be helpful in the current environment. That suggests markets may need to rely more heavily on incoming data and less on explicit guidance from the Fed.

The statement also leaned hawkish, describing the U.S. economy as solid, acknowledging uncertainty, and remaining clear that inflation is still above the Fed’s 2% target rate. The Committee also emphasized its commitment to restoring price stability.

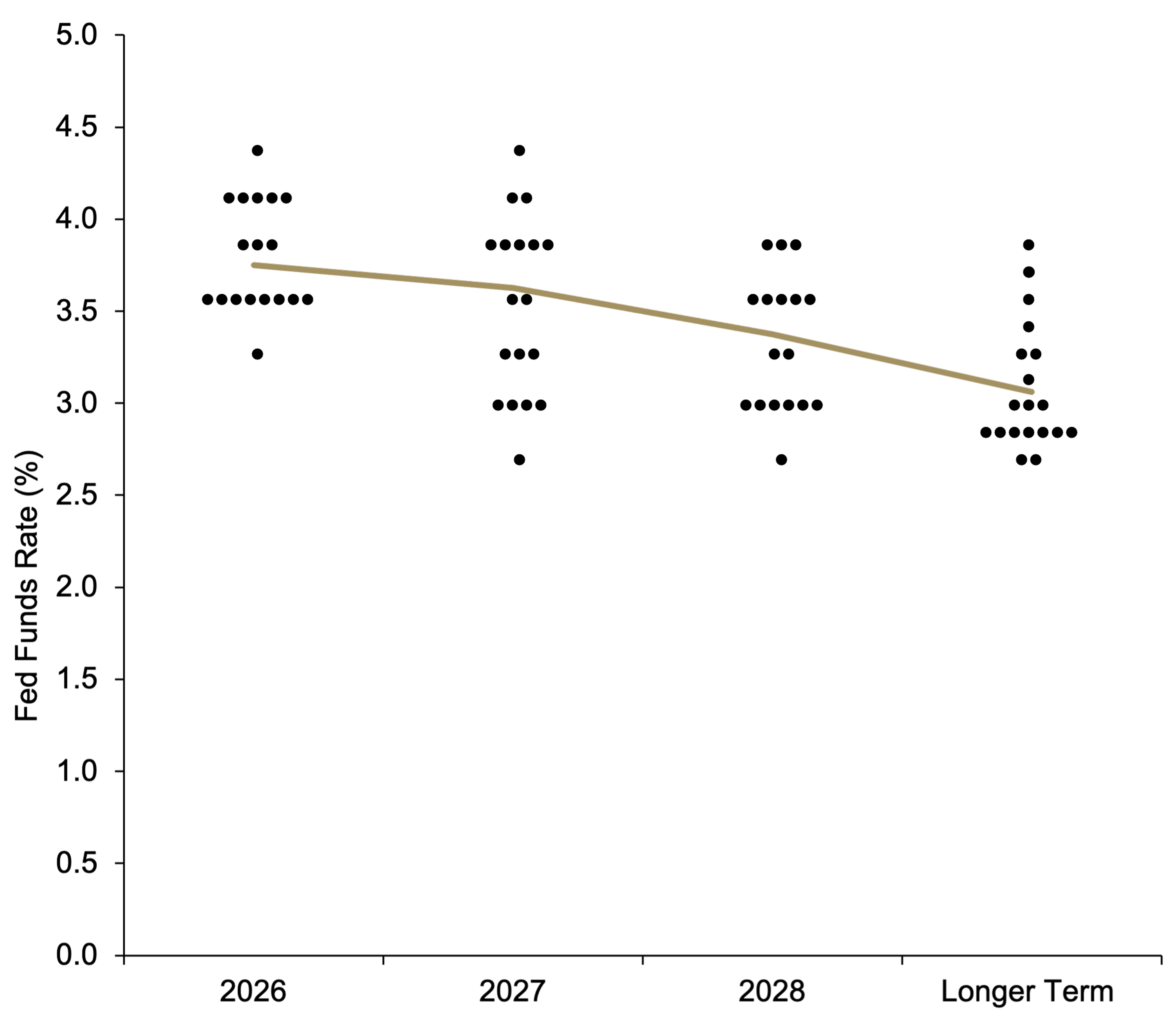

Assessing The Dot Plot

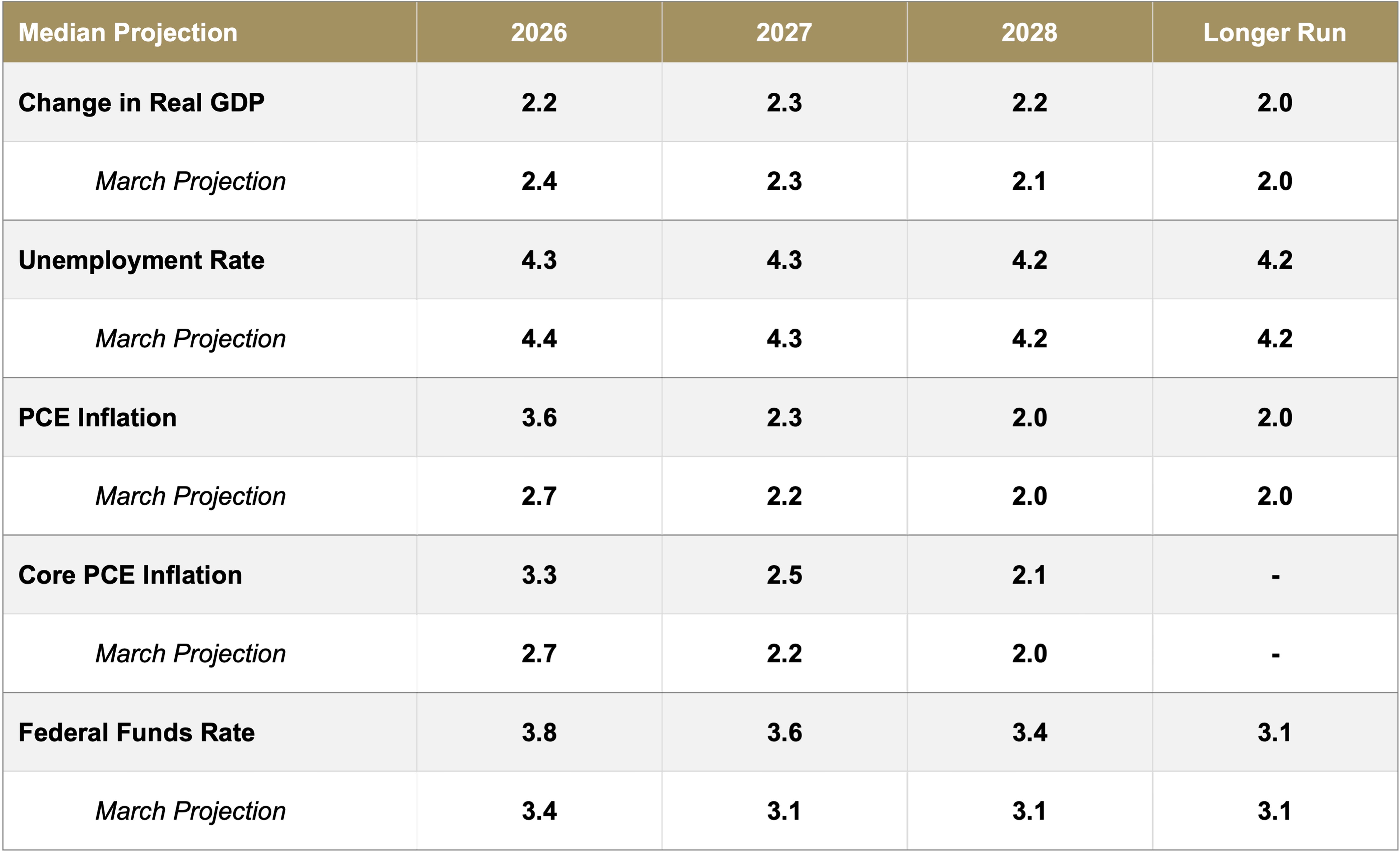

The updated Summary of Economic Projections (SEP) also drew market attention. Chair Warsh did not submit his own expectations about the fed funds rate, (a “dot” in the dot-plot survey of FOMC members), consistent with his previously expressed skepticism about the SEP and dot plot framework. However, the other 18 Committee participants did submit projections, and those dots shifted in a more hawkish direction. Several participants projected at least one rate hike by the end of 2026, while only one participant projected a rate cut. That moved the median dot higher compared with the March 2026 projections, when the median still implied a cut by year-end.

At the same time, the projections were more nuanced than the immediate market reaction suggested. While the 2026 dots showed the possibility of near-term tightening, the 2027 and 2028 projections suggested that some of that tightening could later be reversed. In other words, the Committee seemed to be acknowledging a potential near-term inflation challenge but not necessarily signaling the start of a sustained hiking cycle.