Other underwriting factors that should be considered include: less cyclical industries, companies with stable or growing free cash flow, durable competitive advantages, strong management teams, and sponsors or owners with a record of supporting their businesses.

EBITDA can be a useful shorthand for profitability, but it is not cash. Free cash flow is what supports interest payments. Loan-to-value, meanwhile, helps frame the margin of safety around principal repayment. A lower loan-to-value means the lender is advancing a smaller portion of the company’s value, which can provide a cushion if operating performance weakens, or market valuations decline.

This is why we believe the current environment favors active, experienced private credit managers. More deal flow and wider spreads are constructive, but the most durable advantage may come from better documentation, more conservative leverage, and the time to conduct stress analysis before capital is deployed.

Three Things We’re Watching in the Second Half

- Portfolio differentiation

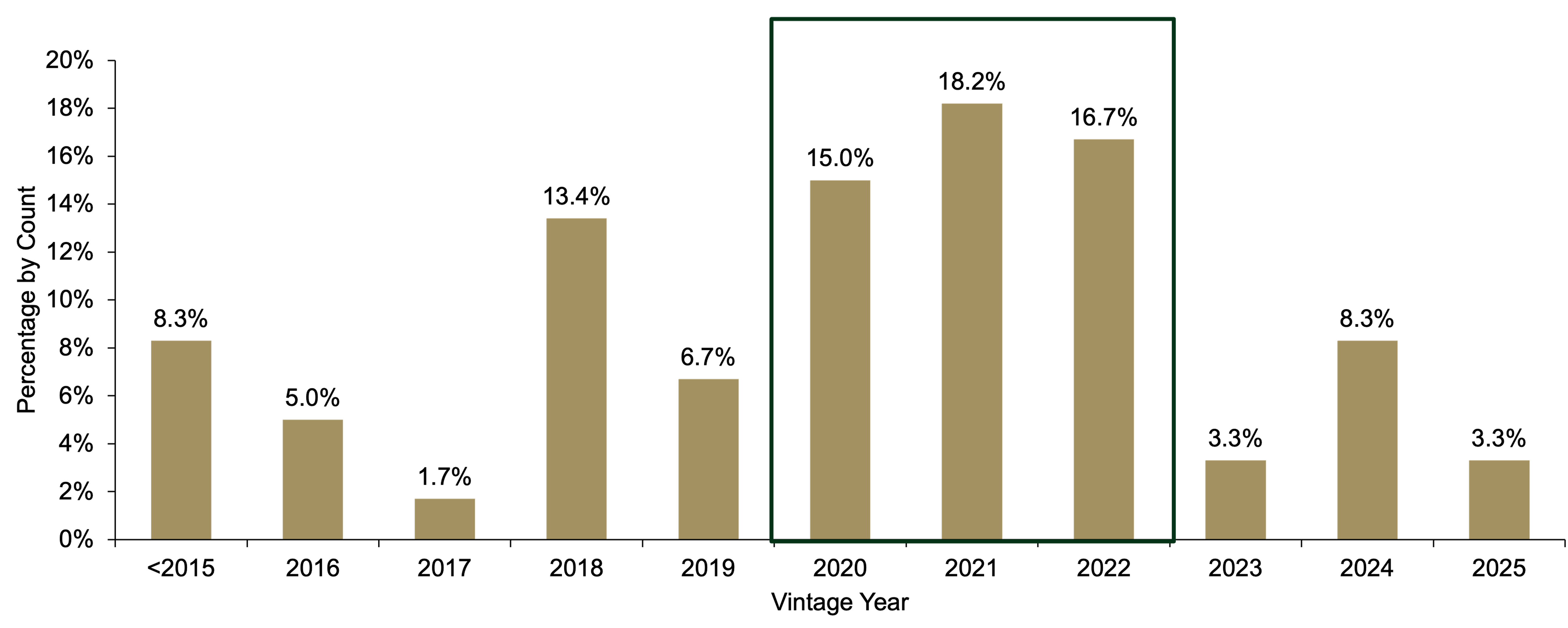

We expect the gap between stronger and weaker portfolios to become more visible as the year progresses. Non-accruals, PIK usage, sector concentration, and 2021-2022 vintage exposure should remain important indicators. We are already seeing signs of greater differentiation, particularly in portfolios with exposure to older vintages and more aggressively financed software-related credits. In our view, this is not a broad indictment of private credit, but rather evidence that manager discipline, sector selection, and underwriting standards are beginning to matter more.

- Dry powder versus redemption pressure leading to portfolio divergence

We are also monitoring whether redemption pressure in certain vehicles widens the gap between managers that may take advantage of today’s improved lending conditions and those that may be more constrained by existing portfolio conditions. From a new-lending perspective, less capital available to compete for deals can improve pricing and structure for managers with dry powder. But redemptions can also change the composition of affected portfolios. If healthier, more liquid loans repay or roll off first, the remaining portfolio may have a higher percentage of non-accruals or PIK loans, even if the absolute number of challenged credits does not change. That dynamic could contribute to additional headline risk and further manager dispersion.

- Stronger credit structures with attractive spreads

Finally, we are watching whether recent improvements in loan structure continue. Before meaningful spread widening typically appears, lenders often first see what we would call better defense: fewer PIK requests, less aggressive leverage, more covenants, and stronger documentation. We have seen those defensive features improve in recent months, and we believe that matters more than modest spread widening alone. For lenders deploying new capital today, the most important shift is not just that potential income has improved, but that the underlying credit structure has improved as well.

Bottom Line: Constructive but Selective

We are constructive on private credit but not complacent. The asset class does not require perfect conditions to perform, and periods of volatility can help restore discipline by reminding borrowers and lenders that credit risk must be priced and structured appropriately.

For new capital, the setup appears better than it was six months ago. M&A activity appears to be creating more opportunities to lend. Capital has become more selective. Spreads are wider. Covenants and documentation are improving. And managers with dry powder can be more selective about the credits they choose to finance.

The second half of 2026 is likely to be defined by dispersion. We believe investors should focus less on broad asset-class headlines and more on where managers are lending; how loans are structured; how much free cash flow borrowers generate; and whether portfolios have the right balance of income, downside mitigation, and selectivity. In today’s private credit market, the opportunity is real, but the potential advantage may go to managers who can combine patience with discipline.