Cyclical and secular tailwinds currently exist that provide interesting and compelling investment opportunities for skilled active international and global equity managers. Structural shifts and policy momentum continue to support non-U.S. regions.

Attractive Relative Valuations Persist

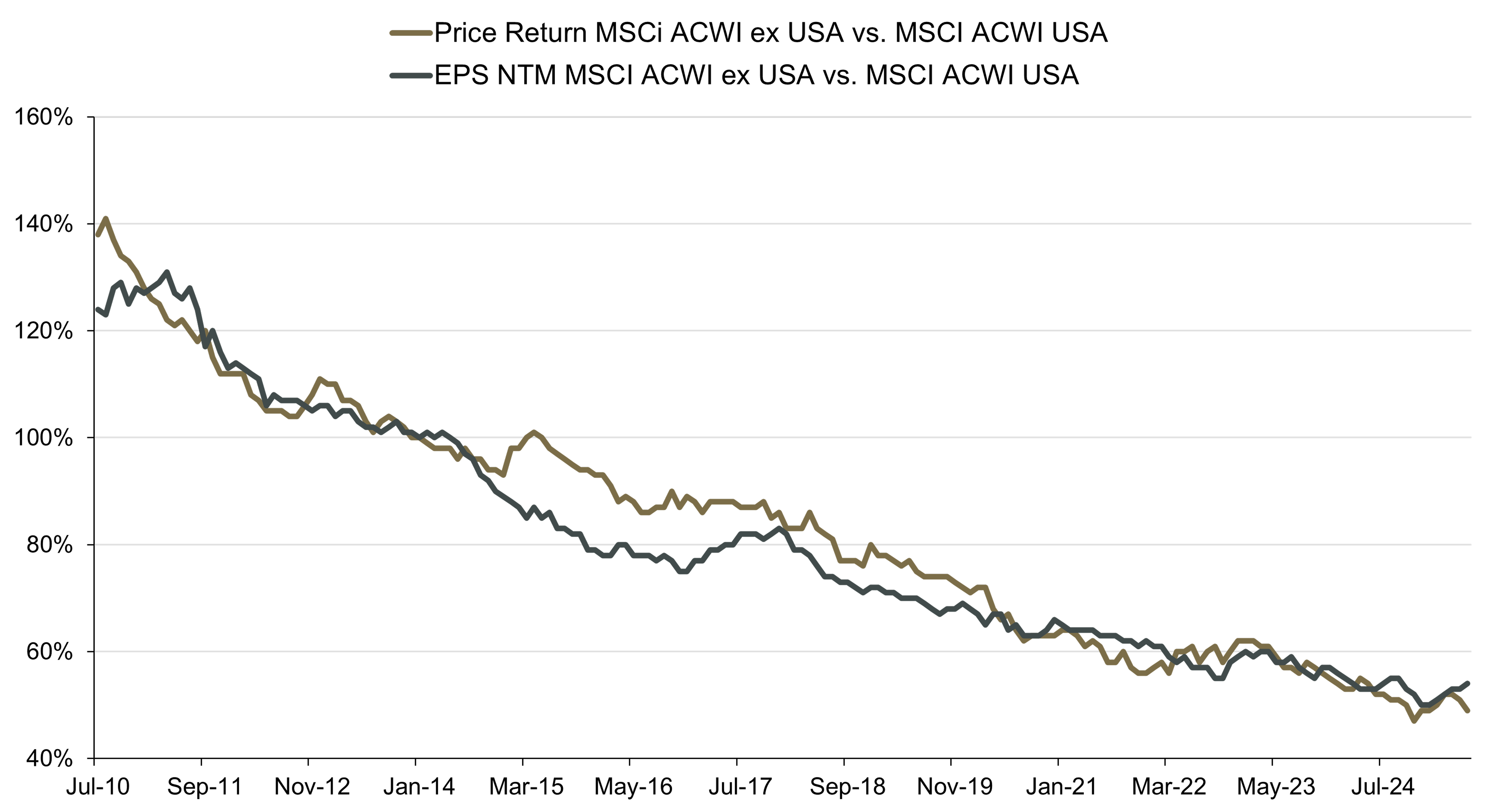

The relative outperformance of U.S. equity markets versus the rest of the world over the years has led to valuations becoming more attractive for the latter. In fact, MSCI ACWI ex-USA valuations versus the S&P 500® are still near historic lows today, even after a strong start this year, sitting at a 36% discount on an NTM P/E basis, according to FactSet. While identifying attractive relative value is important, history suggests that valuation alone might not be a sufficient driver of superior investment returns; a catalyst is often needed to unlock value.

Figure 1. Valuations Still Appear Compelling

MSCI ACWI ex USA price return as a proportion to MSCI ACWI USA price return and MSCI ACWI ex USA EPS NTM as a proportion to MSCI ACWI USA EPS NTM, July 31, 2010-June 30, 2025

Secular and Cyclical Tailwinds for Opportunities

Much like the extraordinary U.S. stimulus was the key to lasting performance after the Global Financial Crisis (GFC), we believe catalysts to drive secular and cyclical growth in non-U.S. equity markets is finally here, after Germany announced expanded fiscal stimulus measures with a $546 billion infrastructure fund and pledged another $500 billion to increase defense spending. This $1 trillion plan provides a tailwind to companies with defense spending exposure, as well as to the industrials and materials sectors, and renewable energy firms.

For context, this combined spending is more than 3x what Germany allocated for its entire post-pandemic stimulus package. Moreover, other European countries have echoed Germany’s commitment to defense spending, including at least seven other European Union (EU) member states. This marks a generational shift in Europe’s commitment to fiscal austerity and dependence on monetary policy to stimulate the economy. As balanced budgets, debt reductions, and limited government stimulus are deprioritized, this could be a turning point for Europe’s economic trajectory.

The rapid expansion of generative artificial intelligence (AI) is driving a surge in global data center construction, which, in turn, is significantly increasing electricity demand. We believe this trend is creating a compelling investment opportunity in both renewable and traditional energy sectors overseas. Countries with abundant solar, wind, hydro, or geothermal resources are likely poised to attract infrastructure investment to power AI workloads, while others may rely on natural gas or other conventional sources to meet immediate demand. As AI adoption accelerates, energy producers and investors could stand to benefit from this structural shift in global power consumption patterns.

The Quality Anomaly: Why it Matters

Supportive tailwinds for growth can lead to increased competitive and operational strengths across a vast opportunity set in international equity markets. While geographic diversification can help mitigate macroeconomic risks, it often overlooks the fact that high-quality companies can outperform regardless of their home market’s performance. Strong fundamentals tend to drive long-term value creation, especially during periods of volatility or economic transition. By prioritizing company-specific strength over broad regional bets, investors can better capture sustainable growth and reduce exposure to systemic risks tied to political, fiscal, or monetary shifts in a given country or region.

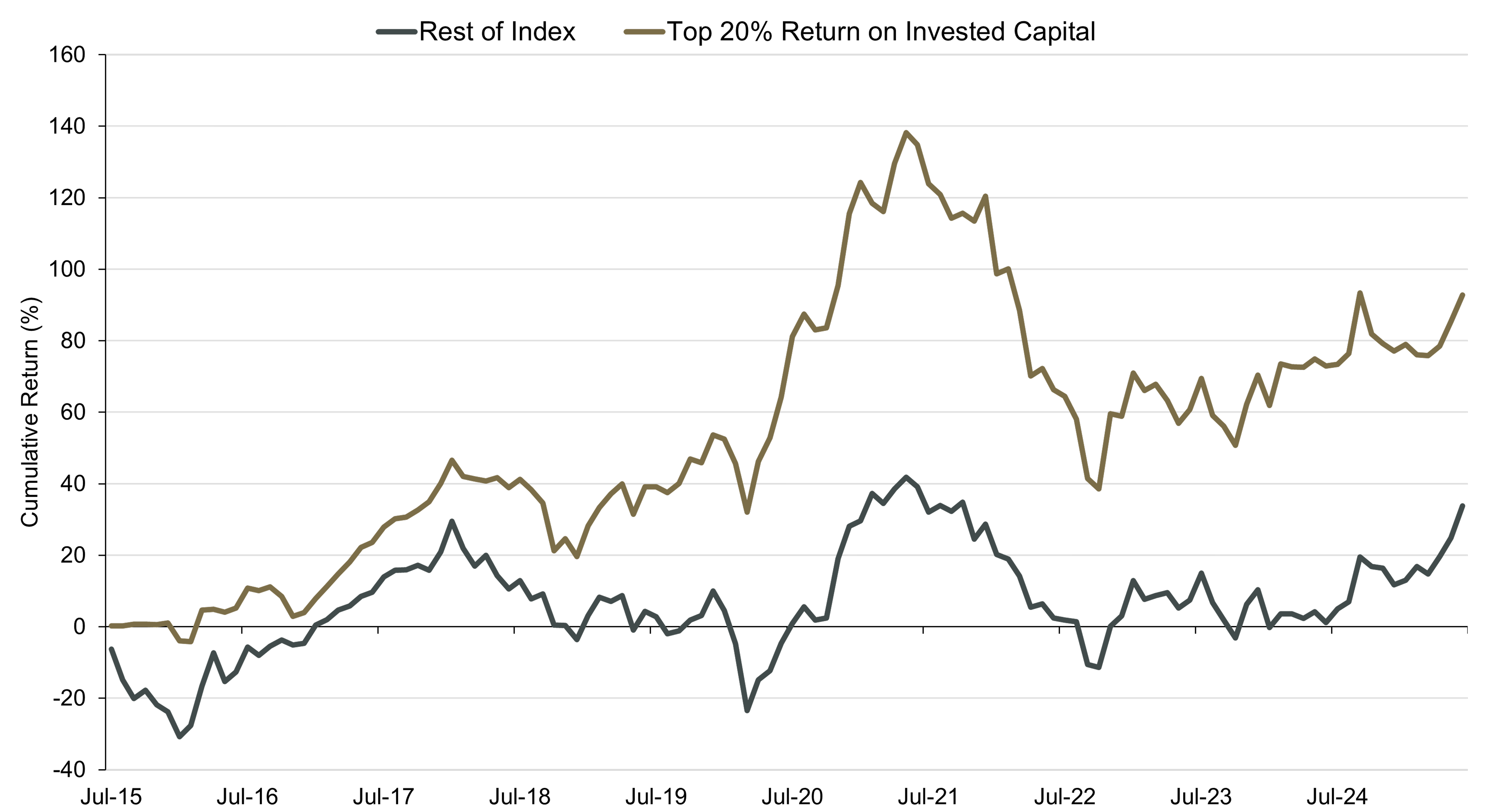

By focusing on businesses with sustainable competitive advantages—such as strong pricing power, dominant scale, or operational complexity—that tend to exhibit quality traits, a selective global equity approach can uncover investment opportunities with the potential to generate attractive alpha. Those traits include high returns on invested capital (ROIC), free cash flow, and substantial margins—characteristics of companies with a strong competitive “moat.” In fact, we have found that over the last decade, the top quintile (top 20%) segment of the MSCI ACWI ex-USA Index, based on annual ROIC growth, outperformed the rest of the index by 59% (see Figure 2).

Figure 2. Quality Stocks with High ROIC Have Outperformed

MSCI ASWI ex USA top 20% ROIC segment cumulative return and the rest of the index, July 31, 2015-June 30, 2025

Earnings Power to Sustain Robust Quality Metrics

It is critical to identify specific operating advantages that allow firms not only to exhibit strong quality indicators but also sustain them through earnings power. To do that, we believe that it’s vital to distinguish between a company’s exposure to secular tailwinds and its internal operating strengths. Secular trends—such as the rise of AI, increased defense spending, and global power demand—can create favorable conditions for entire industries, lifting many companies regardless of their individual quality. However, not all firms benefit equally.

A company’s ability to capitalize on these trends depends heavily on its management’s strategic decisions, execution capabilities, and control over market expectations. By separately evaluating these internal factors, such as management effectiveness, operational efficiency, and adaptability, investors can identify businesses that are not just riding a wave but actively steering their success. This distinction helps uncover companies with true operating strength, which are more likely to sustain performance even as external tailwinds shift.

Summing Up

With such a vast and diverse universe, we believe that a selective, quality-focused approach to navigating international markets can identify companies with competitive strengths, while active management teams with broad research and security valuation capabilities may be particularly well positioned to capitalize on the trends that could drive future growth across global equity markets. The team at Lord Abbett dedicated to seeking global and international equity investment opportunities represents a deep and experienced platform with the resources and disciplined investment approach designed to potentially identify opportunities for long-term alpha generation.