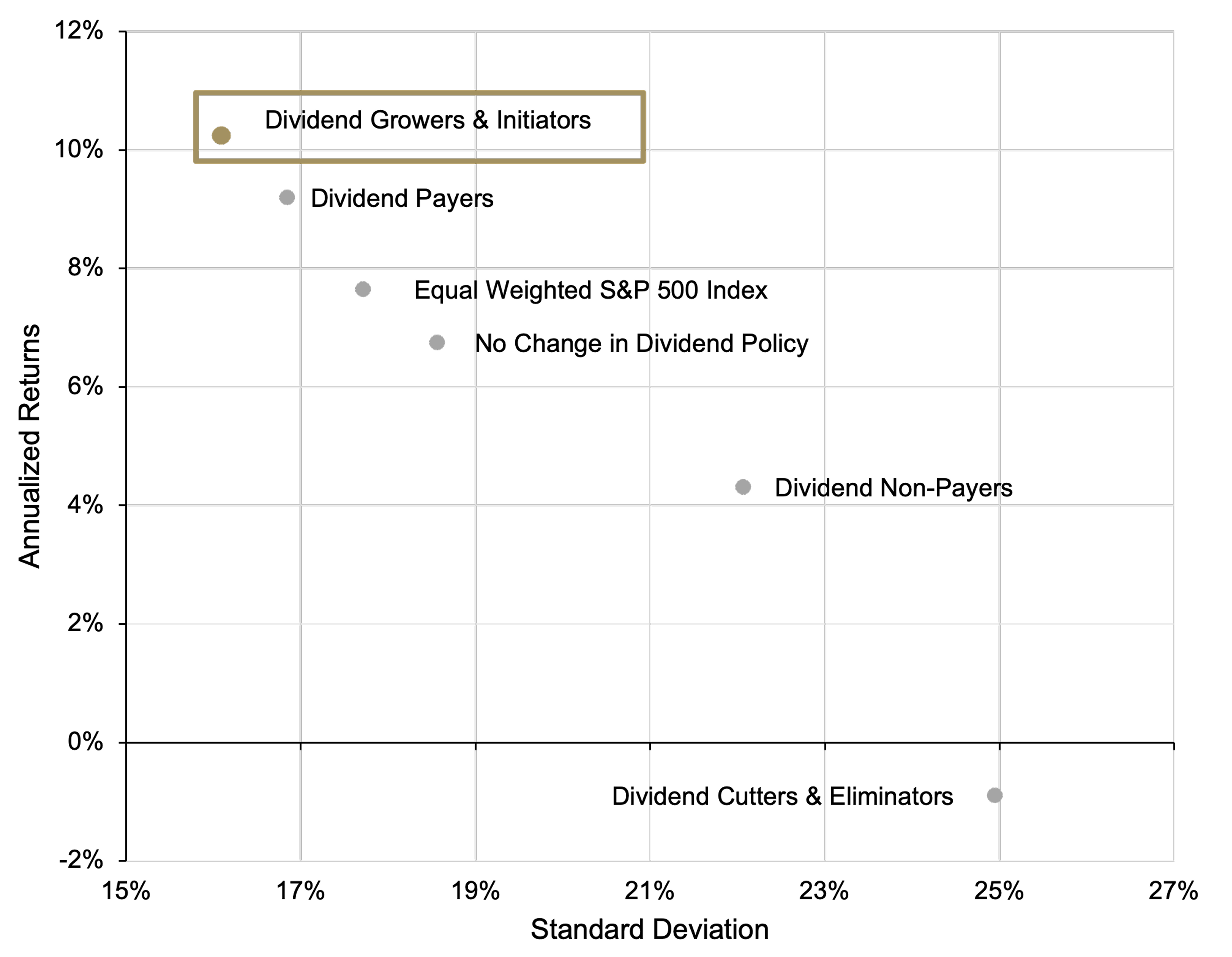

Dividend growth investing starts with a simple but powerful idea: companies that consistently grow their dividends often have the financial strength, cash-flow discipline, and shareholder focus that investors value over time. A long-term study from Ned Davis Research helps illustrate that point. Over the 50-plus-year period from January 1973 through December 2025, dividend growers within the S&P 500® Index generated higher annualized returns with lower volatility than dividend payers that did not grow dividends, dividend non-payers, and dividend cutters.

Figure 1. Dividend Growers Have Offered Higher Returns with Less Volatility

Average annual returns and volatility (standard deviation) for the S&P 500® Index, January 31, 1973–December 31, 2025

Source: Ned Davis Research. Latest available historical data.

Dividend policy: A stock is classified as a dividend payer if it paid a cash dividend any time during the previous 12 months; a dividend grower if it initiated or raised its cash dividend at any time during the previous 12 months; and a non-dividend payer if it did not pay a cash dividend at any time during the previous 12 months. A company's dividend payments may vary over time, and there is no guarantee that a company will pay a dividend at all.

Standard deviation is a statistic that measures the dispersion of a data set relative to its mean. The higher the standard deviation, the further the observed data are from the mean.

Past performance is not a reliable indicator or guarantee of future results. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees and expenses, and are not available for direct investment.

Dividend policy: A stock is classified as a dividend payer if it paid a cash dividend any time during the previous 12 months; a dividend grower if it initiated or raised its cash dividend at any time during the previous 12 months; and a non-dividend payer if it did not pay a cash dividend at any time during the previous 12 months. A company's dividend payments may vary over time, and there is no guarantee that a company will pay a dividend at all.

Standard deviation is a statistic that measures the dispersion of a data set relative to its mean. The higher the standard deviation, the further the observed data are from the mean.

Past performance is not a reliable indicator or guarantee of future results. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees and expenses, and are not available for direct investment.

That historical relationship is important, in our view. It suggests that the dividend growth universe itself has been an efficient place to look for quality companies—businesses that have historically combined attractive return potential with a more stable risk profile. This efficiency may have led some managers to believe that dividend investing is an area where active management may not add value, and where passive, rules-based strategies may be sufficient. These strategies use screens that may include rules such as a minimum number of consecutive years of dividend growth, U.S. listing status, or yield constraints. While those rules can create a disciplined portfolio, they can also exclude companies with strong fundamentals and meaningful future dividend growth potential.

That is where we believe active management can make a difference. The Lord Abbett Dividend Growth Strategy is not limited to a checklist. Instead, it uses fundamental research and portfolio manager judgment to evaluate whether a company has the willingness and ability to be a long-term dividend grower.

This flexibility allows the Strategy to pursue opportunities that rules-based peers may miss. A company may temporarily pause its dividend growth during an unusual period, fall short of a 10- or 25-year dividend growth requirement, trade outside a U.S.-listed universe, or carry a dividend yield above a passive index threshold. A rules-based strategy may automatically exclude those companies. An active manager can assess whether the exclusion reflects a real risk—or a potential opportunity.

In practice, this flexibility has helped the Strategy invest in companies that rules-based approaches may temporarily exclude despite strong long-term fundamentals and future potential. For example, retailer TJX Companies paused its dividend growth during the COVID-19 shutdown—a short-term disruption that caused many passive strategies to remove the stock, even though the company’s long-term cash-generation and dividend growth ability remained intact.

Similarly, we invested in drugmaker Eli Lilly several years before it met the 10-year dividend growth threshold used by some passive strategies because we believed the company had shown a willingness to boost its dividend alongside the growth in earnings it was experiencing. Both of these examples have been large, positive contributors to our performance over that period and have helped us differentiate ourselves versus our peers These examples illustrate how active management can identify durable dividend growth opportunities that may not yet fit neatly within an index methodology.

We believe the long-term case for dividend growers is strong. But within that already attractive universe, we believe active management can add value by separating durable dividend growth opportunities from companies that merely meet an index rule. In our view, that combination—an historically efficient dividend growth universe plus a flexible, research-driven approach—can be a powerful way for equity investors to pursue equity income, quality, and long-term total return.