Founded in 1929, Lord Abbett has a long-standing legacy in U.S. fixed income and pioneered multi-sector bond investing in 1971 with the launch of the Bond Debenture Fund—one of the first to combine credit sectors like high yield and convertibles. This innovation positioned the firm as a leader with deep expertise that endures today. As we mark 55 years of multi-sector credit investing, we examine the factors supporting a constructive backdrop for credit and highlight historical trends that create attractive opportunities for an active approach that seeks to generate better alpha.

Returns across fixed income sectors can vary significantly from year to year, depending on the macro environment (see Figure 1). In fact, over the past decade, calendar-year performance has shown that no single sector has led or lagged consistently. This variability highlights the importance of diversification and active management, as sector leadership rotates with changing market dynamics. A multi-sector approach allows managers to adapt to these shifts and allocate across credit segments to potentially capture opportunities and mitigate risks as conditions evolve.

Figure 1. Leadership Has Rotated Across Fixed Income Sectors

U.S. fixed income representative index sector calendar year returns, 2015–2025

Source: Bloomberg, ICE Data Indices, LLC, and Morningstar. Data as of December 31, 2025. Index sector returns shown are in percent and include Bloomberg indexes as follows: US Aggregate Bond Index, US MBS Fixed Rate Index, US Corporate Investment Grade Index, US Corporate High Yield Index, US. Treasury Index, US. TIPS Index, and ABS Index. Morningstar LSTA U.S. Leveraged Loan Index used for leveraged loans. ICE BofA All U.S. Convertibles Index used for convertibles. MBS=mortgage-backed security. TIPS=Treasury inflation protection securities. ABS=asset-backed security. Past performance is not a reliable indicator or guarantee of future results. Current performance may be higher or lower than the performance data quoted. This historical table is an illustration of the most commonly used indexes that are representative of various sectors of the bond market and does not depict or predict the performance of any specific portfolio managed by Lord Abbett or any particular investment. Please note not all sectors are represented nor is this an asset allocation recommendation. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

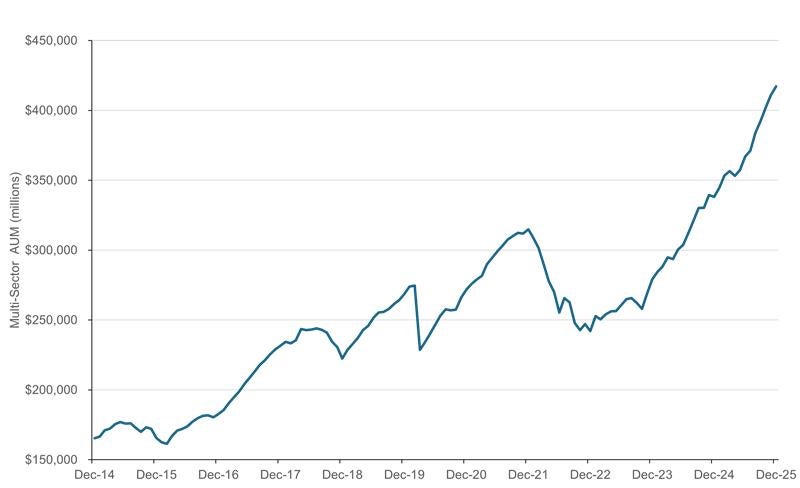

The multi-sector asset class has experienced substantial growth over the past decade, driven by investor demand for diversified credit exposure and flexible strategies. This expansion, shown in Figure 2, highlights the increasing preference among investors for strategies that can dynamically allocate across sectors to capture opportunities and manage risk. Specifically, since interest rates quickly rose in 2022, multi-sector fixed income assets have risen sharply. This reflects the attractive yields offered in credit sectors as well as the historical benefits the investment option has generated for fixed income allocations.

Figure 2. Multi-Sector Fixed Income Assets Have Soared

Morningstar multi-sector category assets, December 31, 2014–December 31, 2025

Source: Morningstar. Data as of December 31, 2025. Most recent data available. The Morningstar Multi‑Sector Bond Category consists of funds that seek income by diversifying across multiple fixed‑income sectors. These funds typically allocate their portfolios among a mix of U.S. government obligations, U.S. corporate bonds, foreign bonds, and U.S. high‑yield debt securities. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Past performance is not a reliable indicator or guarantee of future results. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

A History of Enhanced Returns and Diversification of Rate Volatility

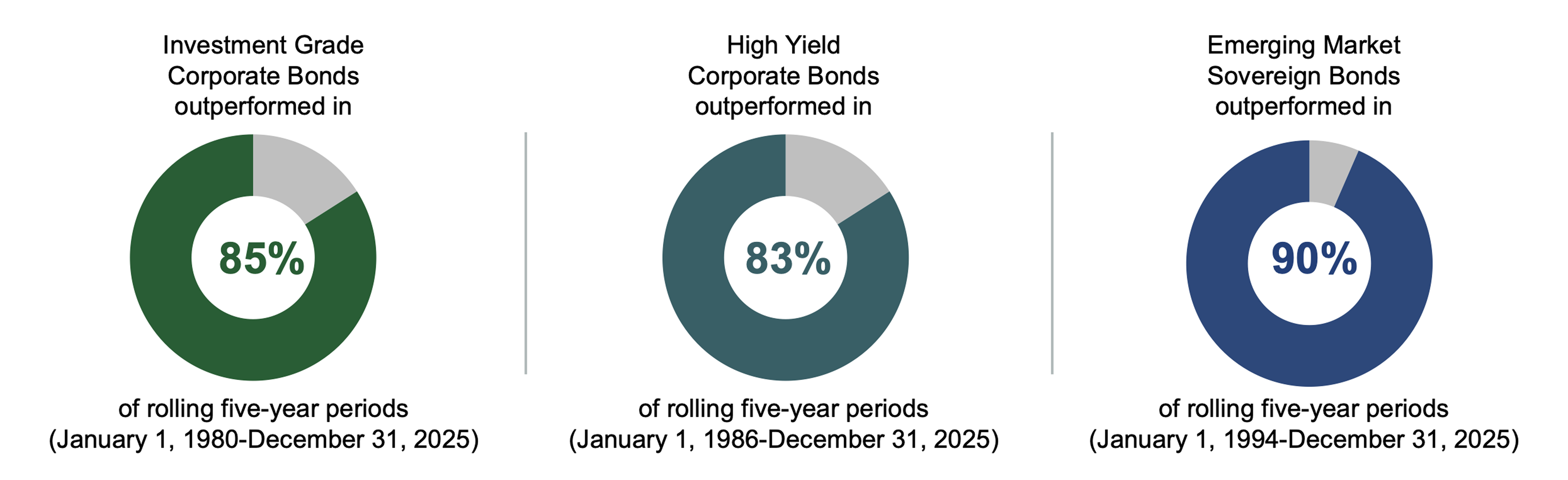

Multi-sector fixed income can also offer the potential for higher returns given its increased flexibility. Over longer time periods, credit-sensitive sectors such as investment-grade corporates, high yield bonds, and emerging market sovereign debt have delivered higher returns than the Bloomberg U.S Aggregate Bond Index (Agg).

Figure 3 shows the percentage of five-year rolling periods in which each credit sector outperformed the Agg. This historical data highlights the value of maintaining a long-term perspective and credit’s persistent ability to enhance returns relative to core benchmarks.

Figure 3. Credit Sectors Have Frequently Outperformed the Agg

Proportion of five-year rolling periods where each credit sector outperformed the Bloomberg US Aggregate Index within each indicated time period.

Source: Bloomberg, ICE Data Indices, LLC and Morningstar, Inc. Data as of December 31, 2025. Most recent data available. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Past performance is not a reliable indicator or guarantee of future results. Investment grade corporate bonds= Bloomberg Corporate Bond Index. High yield corporate bonds=ICE BofA U.S. High Yield Index. Emerging market sovereign bonds=JP Morgan Emerging Market Bond Index Global Diversified (GD). Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

The role of credit in portfolio allocations isn’t just about diversification. After all, it should also be about creating opportunities for income and attractive returns.

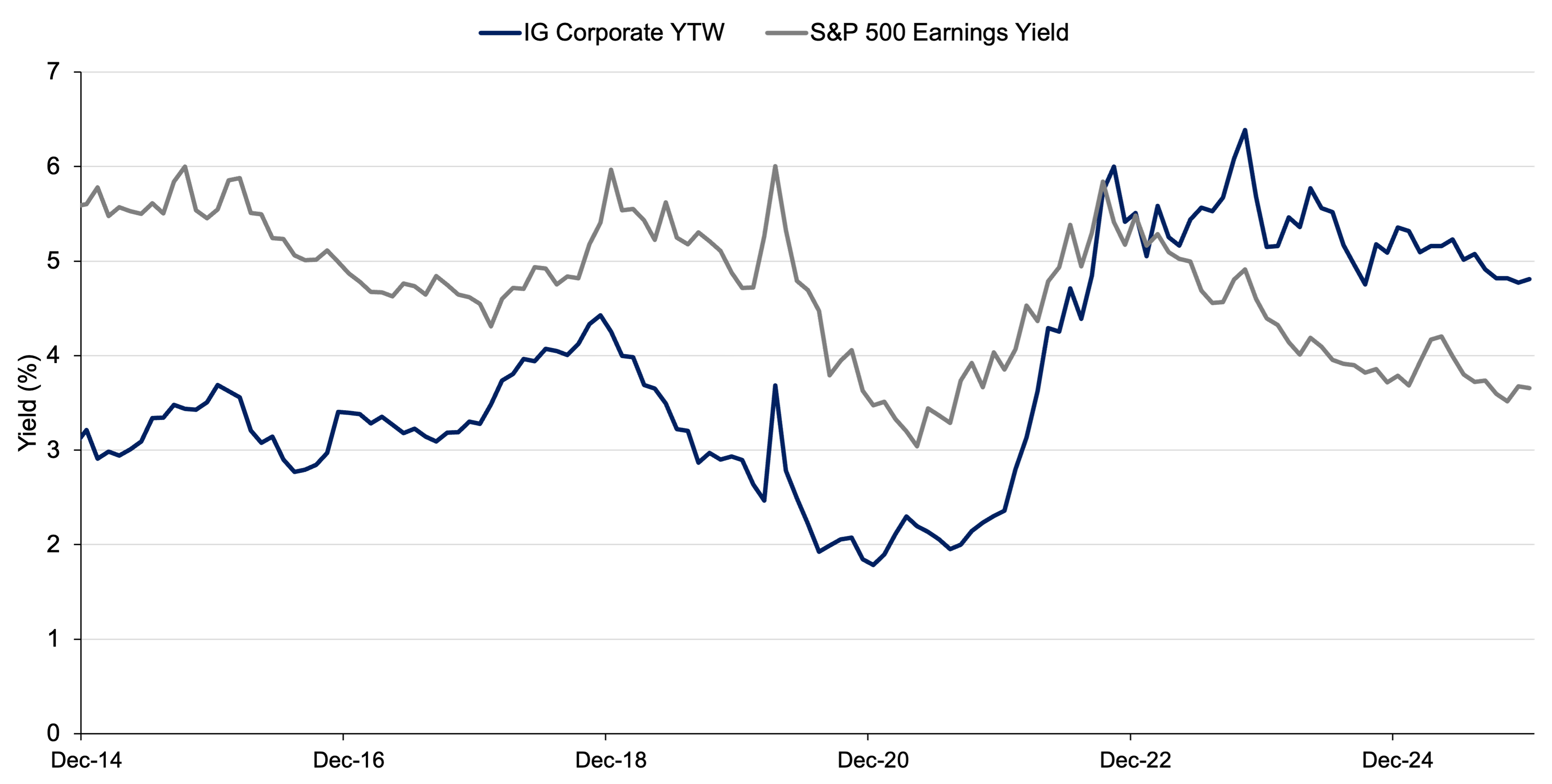

For the first time in decades, starting yields in fixed income are compelling on both an absolute and relative basis. Figure 4 shows the yield-to-worst (YTW) on the U.S. corporate credit index alongside the current earnings yield of the S&P 500® Index.

Figure 4. Historically Attractive Corporate Bond Yields

ICE BofA U.S. Corporate Bond Index YTW and the S&P 500 Index current earnings yield, December 31, 2014–December 31, 2025

Source: Bloomberg and ICE Data Indices LLC. Data as of December 31. 2025. Past performance is not a reliable indicator or guarantee of future results. IG=investment grade. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

A Positive Landscape for a Large and Diverse Asset Class

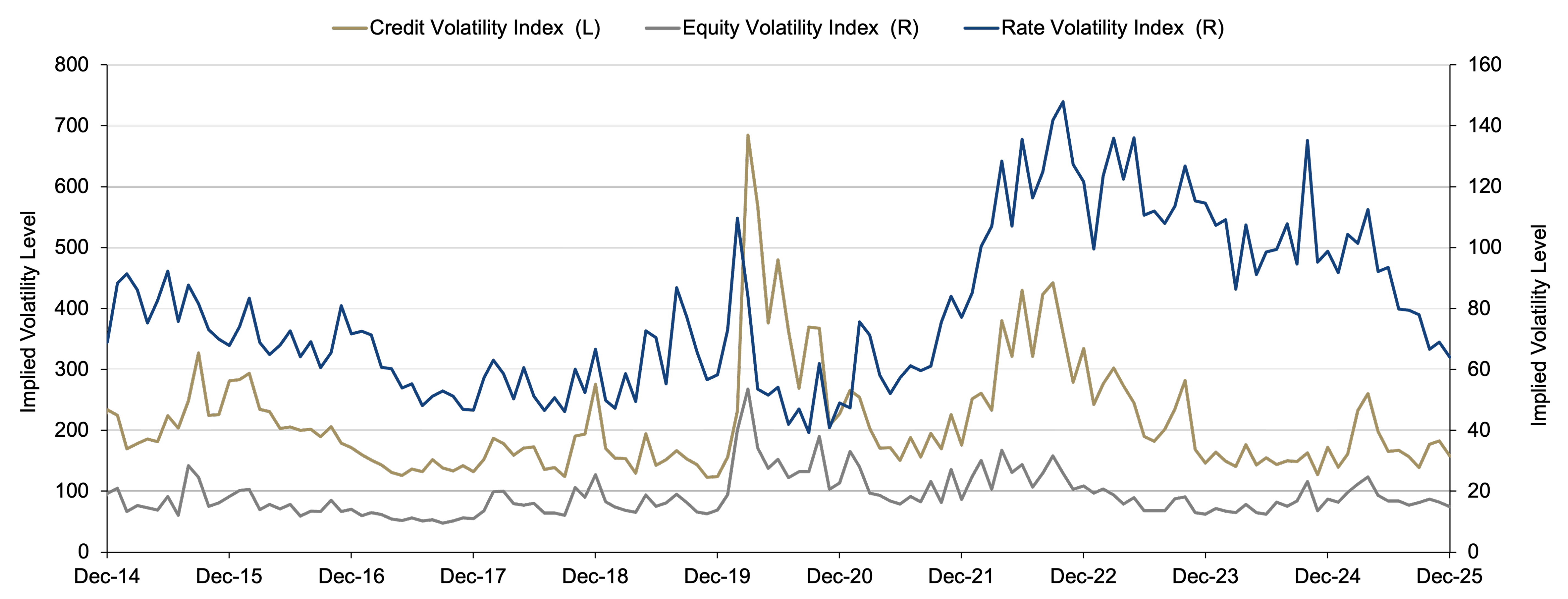

Easing monetary conditions and a supportive economic backdrop of slowing inflation, positive real gross domestic product (GDP) growth, and steady labor markets suggest a constructive environment for risk assets. Yet, despite this healthy backdrop, interest-rate volatility expectations continue to run high, even as volatility in corporate credit and equities has normalized. Figure 5 shows the subdued level of expected volatility for risk assets contrasting sharply with persistently elevated expectations for rate volatility—a dynamic that we think warrants a closer look at credit’s role in fixed income allocations.

Figure 5. Rate Volatility Remains Elevated Relative to History

Expected volatility for credit, equity, and rates, as represented by the Three-Month High Yield VIX, VIX, and MOVE Indexes, respectively, December 31, 2014–December 31, 2025

Source: Bloomberg. Data as of December 31, 2025. The ICE BofA MOVE Index measures U.S. bond market volatility by tracking a representative basket of over the counter (OTC) options on U.S. interest-rate swaps. The index tracks implied normal yield volatility of a yield-curve weighted basket of at-the-money one-month options on the two-year, five-year, 10-year, and 30-year constant maturity interest-rate swaps. The VIX Index is the Chicago Board Option Exchange’s (CBOE) Volatility Index that tracks the stock market's expectation of volatility over the coming 30 days based on S&P 500 index options. The CBOE Three-Month High Yield Volatility Index measures the expectation of high yield bond volatility over the coming three months. Past performance is not a reliable indicator or guarantee of future results. The historical data shown in the chart above are for illustrative purposes only and do not represent any specific portfolio managed by Lord Abbett

This perspective also aligns closely with our investment philosophy: Forecasting interest rate movements is inherently difficult, while credit markets offer an expansive opportunity set and multiple independent levers for skilled multi-sector managers to add value.

Summing Up

The multi-sector asset class has experienced substantial growth over the past decade, driven by investor demand for flexible strategies.

In today’s environment, where interest-rate volatility remains elevated despite a constructive economic backdrop, credit may offer meaningful advantages for fixed income allocations. Combined with attractive starting yields and the prospect for higher long-term returns, credit-sensitive sectors within a multi-sector approach offer a dynamic landscape for experienced managers to add value. Skilled credit managers can leverage deep research, sector rotation, and security selection to help capitalize on opportunities and manage risk across changing market conditions. For investors seeking income, return potential, and resilience, a multi-sector credit approach may serve as an important component of a well-constructed portfolio.