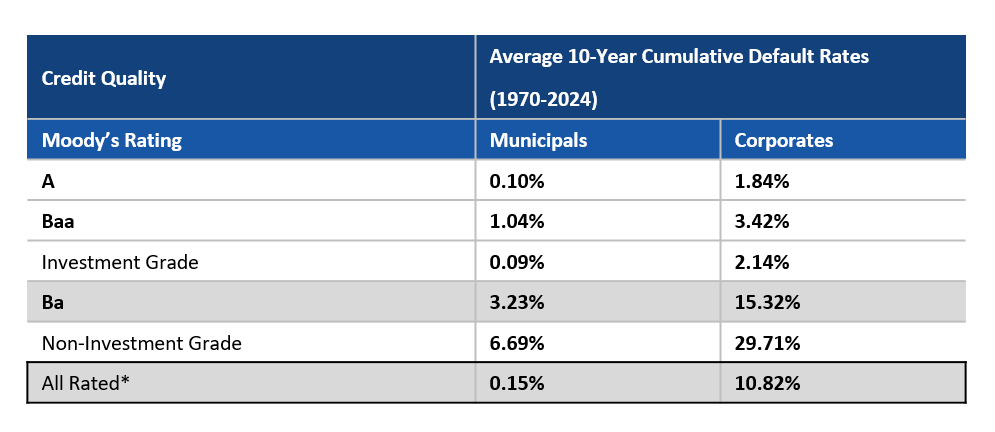

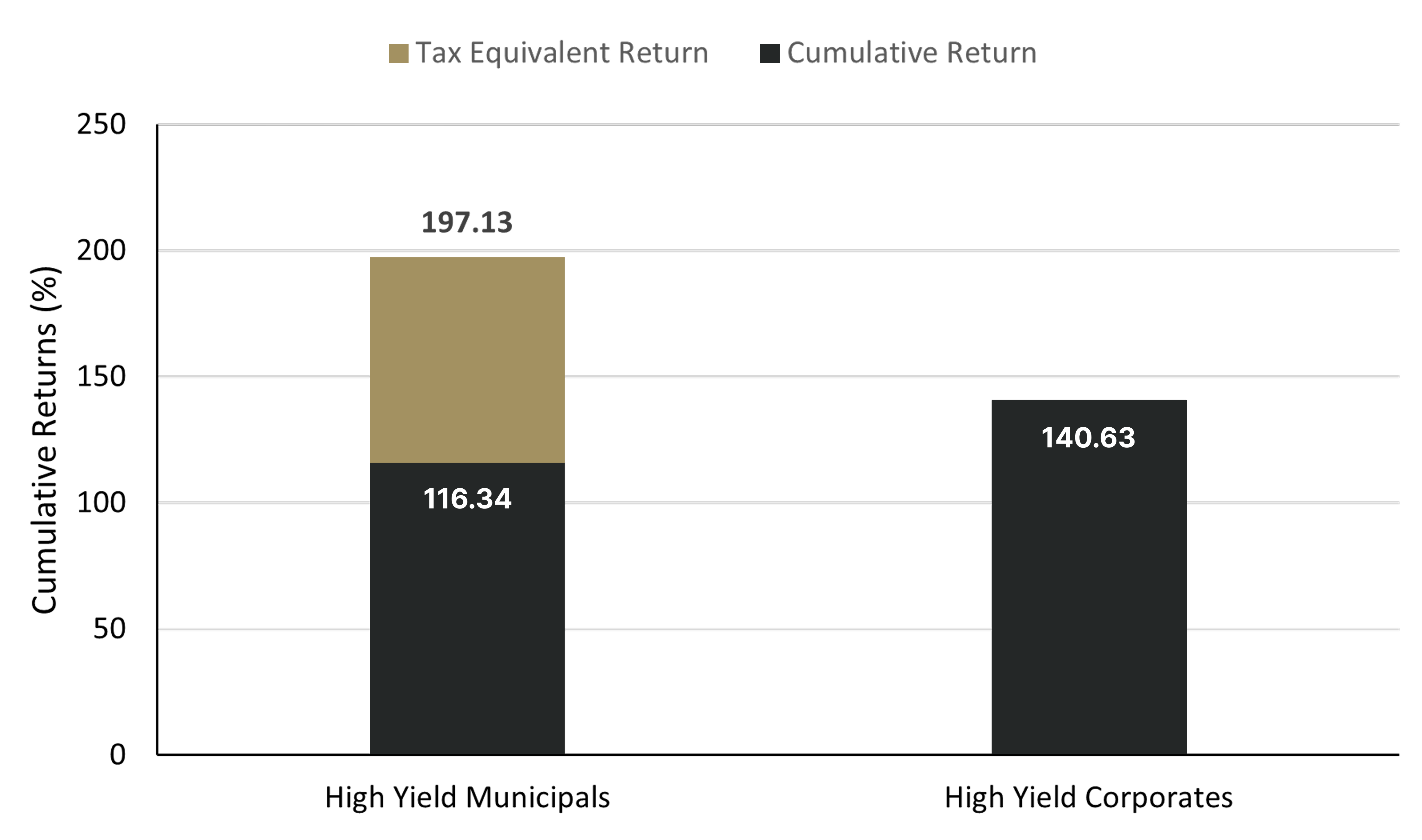

A Deeper Dive into Historical High Yield Muni Outperformance

Academics have hypothesized why this opportunity exists. Most theories are rooted in the inefficiencies of the market and the dominance of individual rather than institutional investors in parts of the municipal market, due to the tax exemption that affects various investors differently and does not benefit institutions as much.

How do these differences play out? Institutional investors, who are at most taxed at roughly half the rate of the highest-earning individuals, tend to be less involved in the tax-exempt market compared to taxable bond markets. Furthermore, municipal investors who receive the maximum tax benefit are predominantly higher earning and potentially more financially conservative individuals. They often do not want to take as much credit risk to achieve an attractive, higher level of tax-free income and prefer to take more risk in other investment opportunities.

So, with a lower prevalence of more sophisticated investors and above-average concentration of cautious buyers, these lower-quality muni investments, which require more skill to evaluate, may receive less attention meaning lower demand. Geography may also play a role, as some retail investors might only be interested in bonds in their home state, given the exemption from state tax as well, further segmenting the market. In addition, financial media outlets typically focus more attention on corporate issuers, so there is less information flowing to individual investors, which makes it harder for them to understand the investments. Finally, liquidity may play a part here, but factors like active management, diversification, and the correct vehicle can help mitigate some of this.

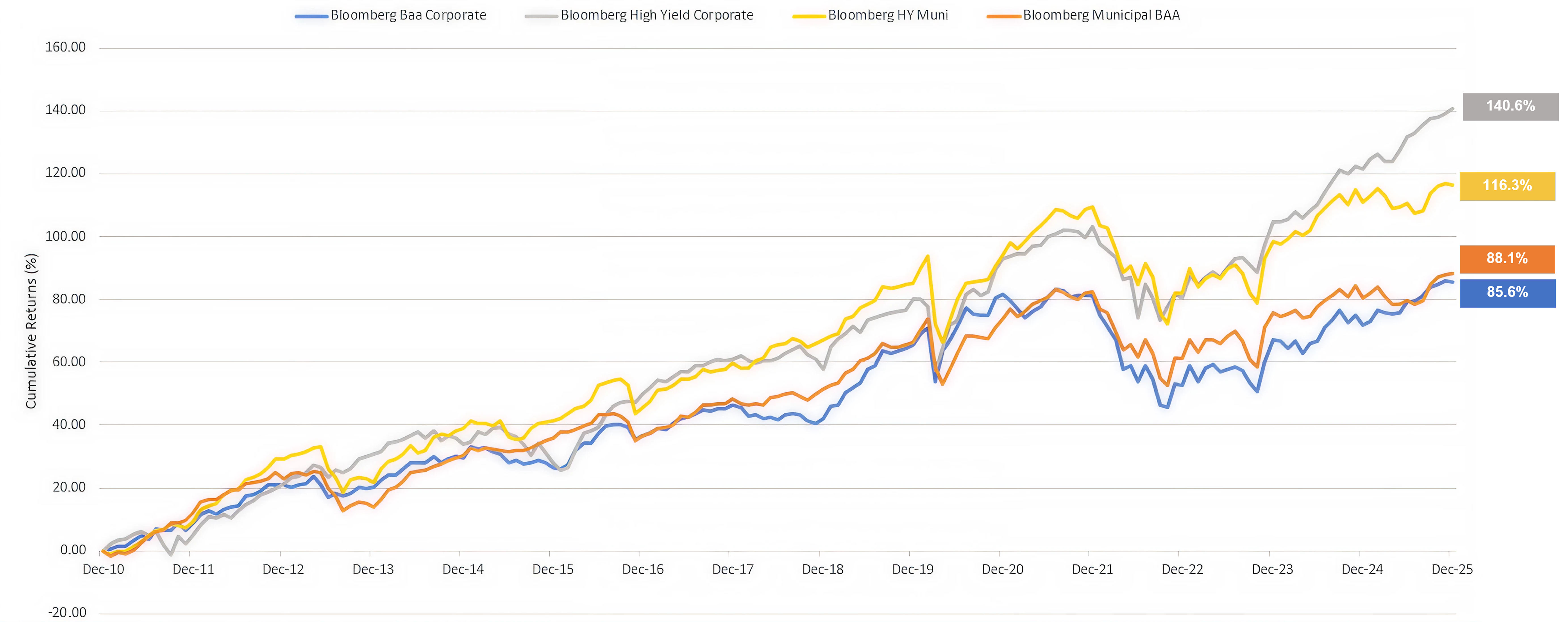

One final note about high yield munis’ historically attractive performance: It has been achieved throughout various interest-rate environments, including the rise in rates in the first 10 months of 2022 and their subsequent decline. One approach that has not yielded favorable results has been market timing, where investors sell bonds in anticipation of rate moves. As we have noted in the past, such maneuvers have typically led to underperformance in high yield muni portfolios. History has shown that a long-term orientation, one that eschews market timing, has led to better results for investors in the asset class. Also, high yield municipal bonds do not trade as frequently as their corporate counterparts, so it may be tough to reestablish a bond position, after selling in an effort to time the market.

In this context, high yield municipal bonds may represent a complementary extension of this broader credit allocation for investors seeking tax-efficient income.

The Current Opportunity

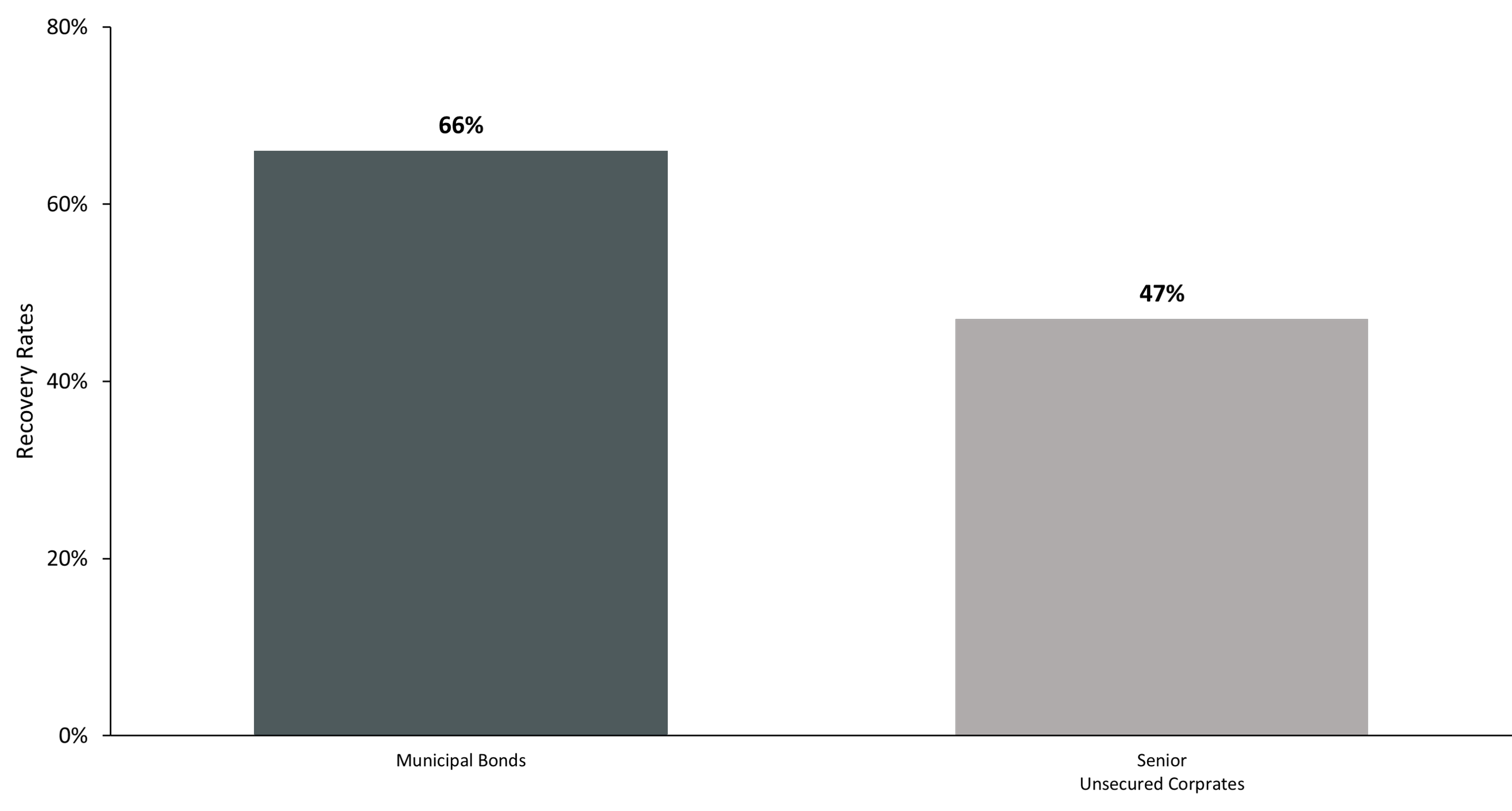

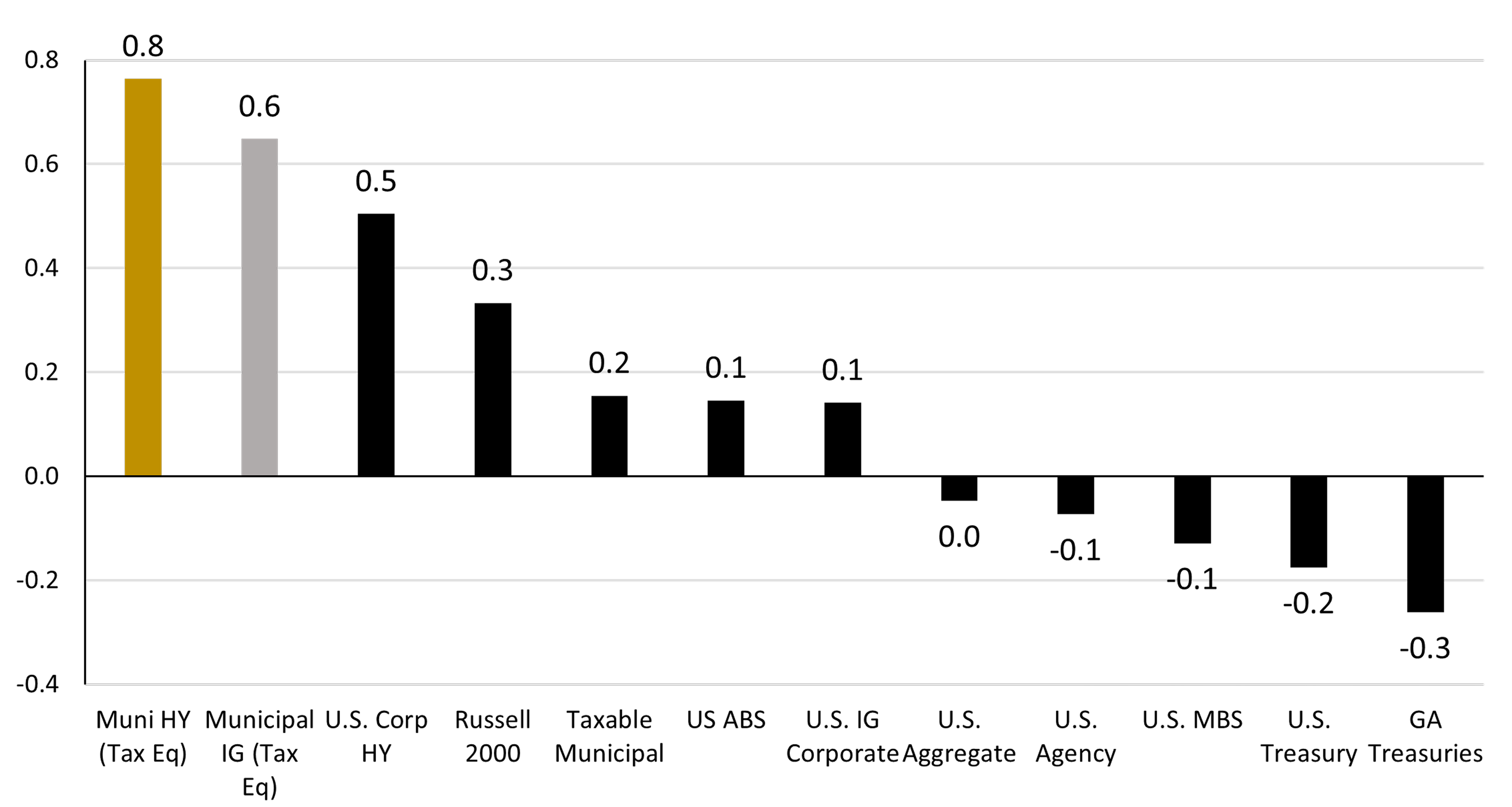

Whatever the reason, these findings illustrate the opportunity in municipal credit and make a strong case for lower-quality parts of the market. We believe lower-rated municipal bonds can play a valuable role within a broader fixed income allocation for high-income investors. This includes portfolios that already include an allocation to taxable high yield, where municipal credit can enhance after-tax income and diversification. The larger risk premium these bonds offer brings an opportunity for high earners to optimize their portfolios, capturing enhanced income and returns while benefiting from the tax advantages inherent to municipal bonds.

We recommend taking advantage of this through an actively managed portfolio run by seasoned municipal investors with decades of experience, diversified by hundreds of these independent credit positions and supported by a deep bench of dedicated research analysts with expertise in the various industries and geographies of the lower-quality municipal market. Additionally, it is important to remember that not all high yield municipal funds are created the same. Many in the High Yield Muni Morningstar category allocate roughly half of assets to non-investment-grade bonds, so investors may not be getting the exposure to lower-rated munis they expect.

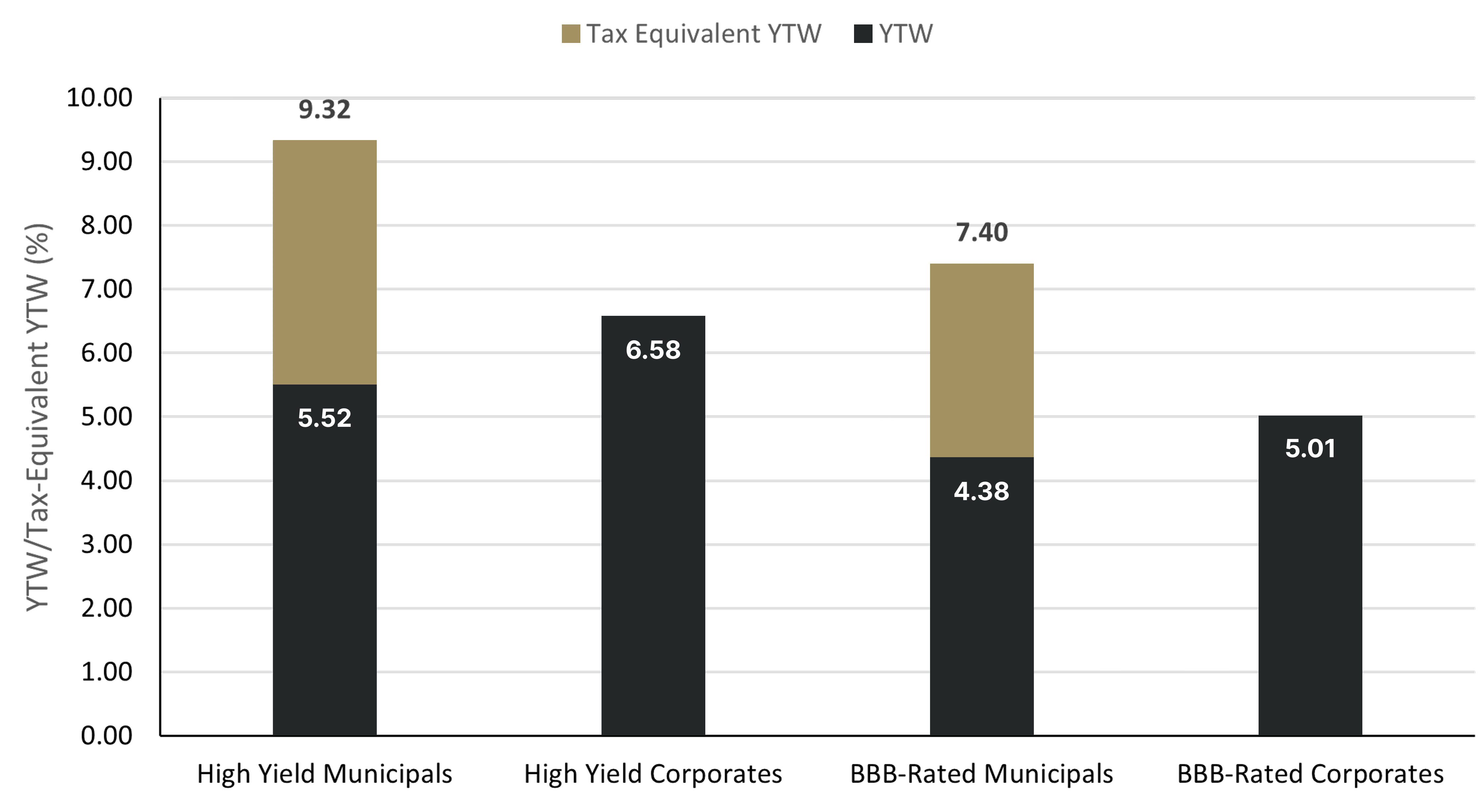

In our view, today’s environment makes for an attractive entry point in the asset class, as the market fundamentals are near the strongest levels in recent history, and yields are just off historically high levels. With the Bloomberg High Yield Municipal Index yielding over 5.5% as of January 31, 2026, this brings a tax-equivalent yield approaching double digits. In other words, an investor locking in today’s attractive yields on lower-rated municipal bonds has the opportunity to position their portfolio to capture attractive income and strong risk-adjusted return potential.