Our 2026 year-ahead outlook was entitled “Riding the Tailwinds,” and the equity market was one of the prime beneficiaries of the favorable conditions we saw back in December. U.S. economic growth was healthy, with real gross domestic product (GDP) at around 2% with an upward bias. Inflation, as measured by the U.S. consumer price index, was moderating, having settled into an area below 3%, well off the post-pandemic highs reached in 2022. The labor market was in good condition, with the unemployment rate remaining near multi-decade lows. That favorable backdrop had translated into solid corporate earnings growth, with strong prospects for additional upside in the coming year.

So where do things stand at midyear? Many of those favorable conditions are still intact, in our view, but there are some new challenges that have emerged. And that underscores the theme of our 2026 Midyear Investment Outlook, “Dispersion Favors the Active Opportunity.” The crosscurrents we identify here signal that this will not be a “go-anywhere market.” Investment managers must be able to recognize the changes in the environment and use their expertise to identify the most compelling opportunities for alpha in the months to come, while avoiding areas exposed to negative industry or macro developments.

Through the end of May, the S&P 500® Index had gained over 11%, supported by resilient economic growth, improving corporate profits, the continued growth of artificial intelligence (AI) across the economy, and the resultant spending on the build-out of AI infrastructure. (Past performance is not indicative of future results.) But AI is not the only factor influencing the market. Conflict in the Middle East has contributed to a large increase in energy prices, which could lead to an uptick in inflation and weigh on U.S. economic growth.

Let’s take a closer look at the themes poised to influence the market in the second half of the year.

Earnings Remain a Dominant Factor as Strength Poised to Continue

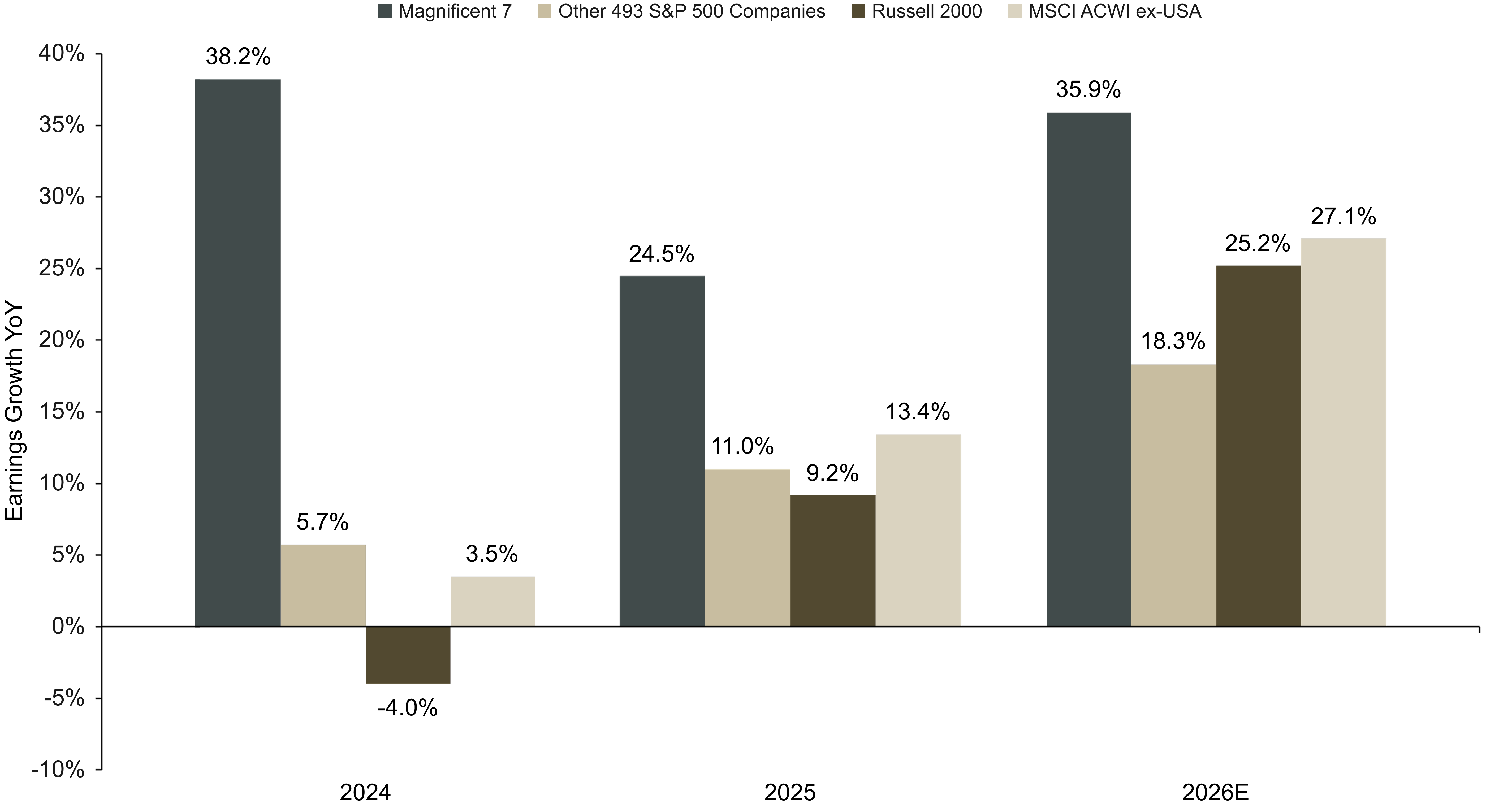

Overall, the earnings picture remains strong. With 97% of S&P 500 companies reporting through the end of May, 85% exceeded analyst earnings forecasts, and 81% exceeded revenue forecasts, both well above long-term averages. S&P 500 earnings growth is now tracking at 28%, year over year for the first quarter, far above the 13% expected earlier in the year (all earnings data presented herein are from FactSet).

Just as important, earnings leadership has broadened beyond the so-called Magnificent Seven tech companies. While these mega capitalization (cap) leaders continue to perform well, earnings growth across the other 493 companies in the S&P 500 has improved meaningfully (see Figure 1). Small cap earnings, which were negative in 2024, turned to strong growth going into 2026. With nearly 95% of the companies in the Russell 2000® Index having reported through the end of May, earnings growth is expected to come in at over 15%, well ahead of expectations at the beginning of the year. Earnings growth has also accelerated outside the United States. This shift signals healthier market breadth and creates opportunities beyond the mega cap market leaders.