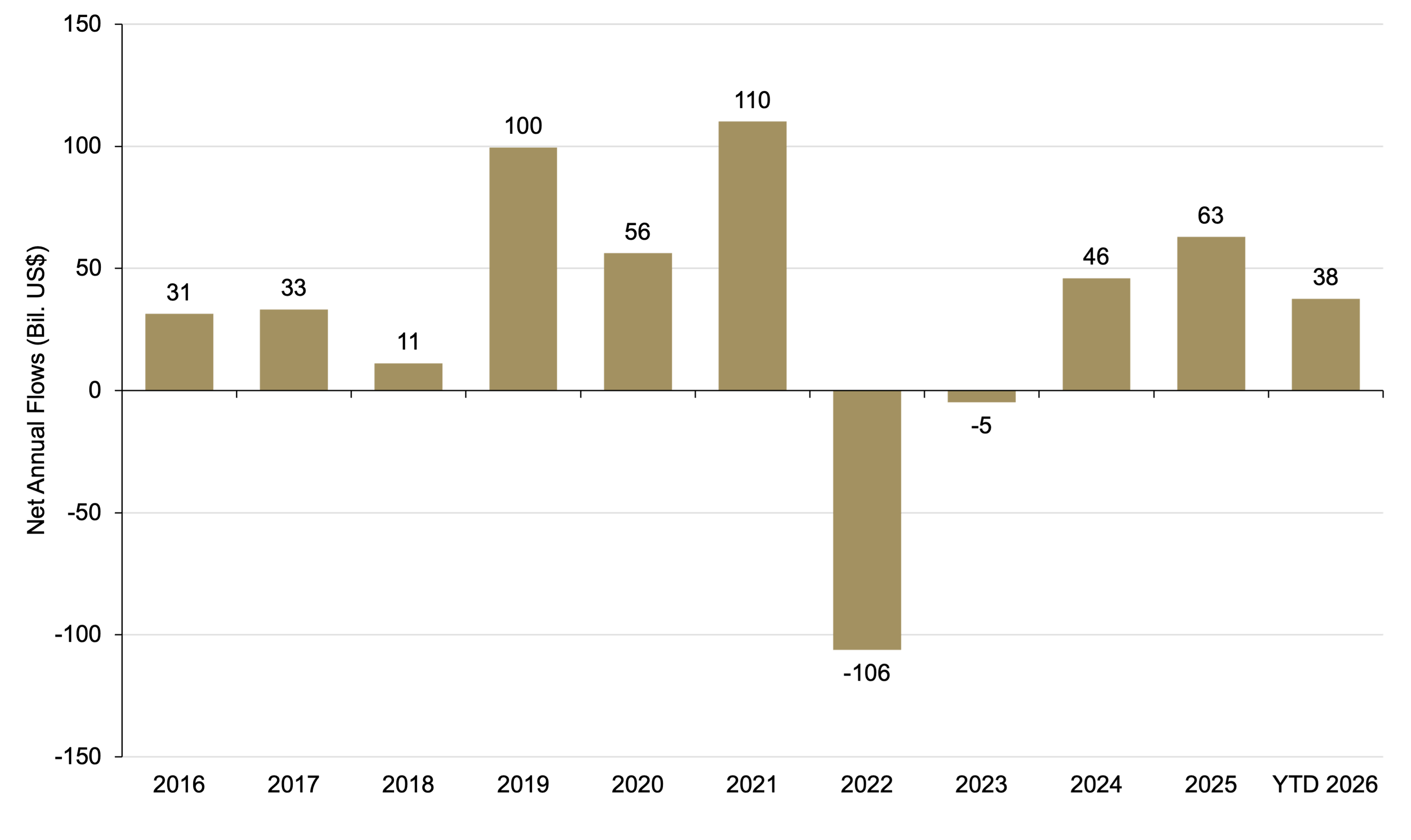

Part of what triggered the change in fund flows was the decision by the U.S. Federal Reserve (Fed) to lower rates near the end of last year. The individual investors who make up over two-thirds of the municipal market holders (based on Fed data) appear to be more comfortable with the asset class when interest rates are stable or declining. While there is much discussion about the direction of Fed policy at mid-2026, we would note that the likelihood of a significant upward move in rates seems low, which represents a potential positive for the municipal bond market. (Note that there is no guarantee that these conditions will continue in the future.)

We have also observed that demand for municipal bonds from separately managed accounts continued to be extremely strong through the first five months of 2026, especially for bonds with maturities of 10 years or shorter.

Muni Credit Quality Reflects Overall Strength and Stability

Credit fundamentals across the municipal market remain broadly stable, in our view, supported by conservative budgeting practices by state and local governments, strong reserve balances, and manageable debt burdens across many state and local issuers.

While investors continue to focus on broad areas like sectors, regions, or states for signs of fiscal stress, we currently view risks as largely issuer-specific rather than systemic. Even among issuers that periodically become the focus of market concern or political headlines, underlying credit fundamentals generally remain sound.

In the case of U.S. states, rainy day fund balances—financial reserves that could be used to cover state operations if revenues come in below expectations— remain near historically high levels, potentially offering a meaningful cushion against economic headwinds. Though there has been some moderation in overall fund levels from the post-pandemic period of budgetary strength, a recent report from the Pew Charitable Trusts noted that most states still have stronger rainy-day funds than they did just before the COVID-19 pandemic. We will continue to monitor tax collections and state budget developments amid signs of slowing economic growth and rising operating costs. In general, though, we have observed states paying greater attention to maintaining higher rainy-day fund balances.

Finally, we would like to emphasize two points we made earlier this year about the municipal bond sector following the market volatility that ensued at the start of the U.S.-Iran conflict:

- As a domestically oriented asset class with limited direct exposure to global supply chains or energy production, municipals are generally less sensitive to geopolitical shocks than many other sectors.

- The essential-service nature of most municipal revenue streams, including utilities, healthcare systems, transportation infrastructure, and education, has historically supported stability through the full range of economic cycles.

Positive Signals for High Yield Munis

High yield municipal fundamentals also remain constructive, with default activity continuing to run at relatively low levels. According to Moody’s, long-term cumulative default rates for high yield municipals have historically remained well below those of comparable corporate bonds.

Importantly, municipal credit deterioration often develops gradually, allowing disciplined credit research to typically identify potential stress signals before default occurs. At present, we continue to observe limited signs of broad-based distress across the high yield market.

Meanwhile, though there have been numerous headlines about the compression in spreads for taxable high yield bonds, we would note that spreads for high yield munis are tougher to quantify, even as some analysts state that they might be slightly tighter than average. Basic spread analysis would suggest that current spreads are near average levels, but there is often a huge discrepancy between different parts of the high yield muni market. For example, there are some bonds in the high yield muni index with yields in the 5% range, but there are many others in the 6% to 7% range or even higher, making it hard to come up with one opinion about spreads. There are actually several areas of the market that are still attractive in terms of credit spreads, in our view.

Supply in the high yield space has not kept up with other areas of the muni market, given today’s higher rates. But demand remains positive. This augments the favorable technical backdrop for high yield munis.

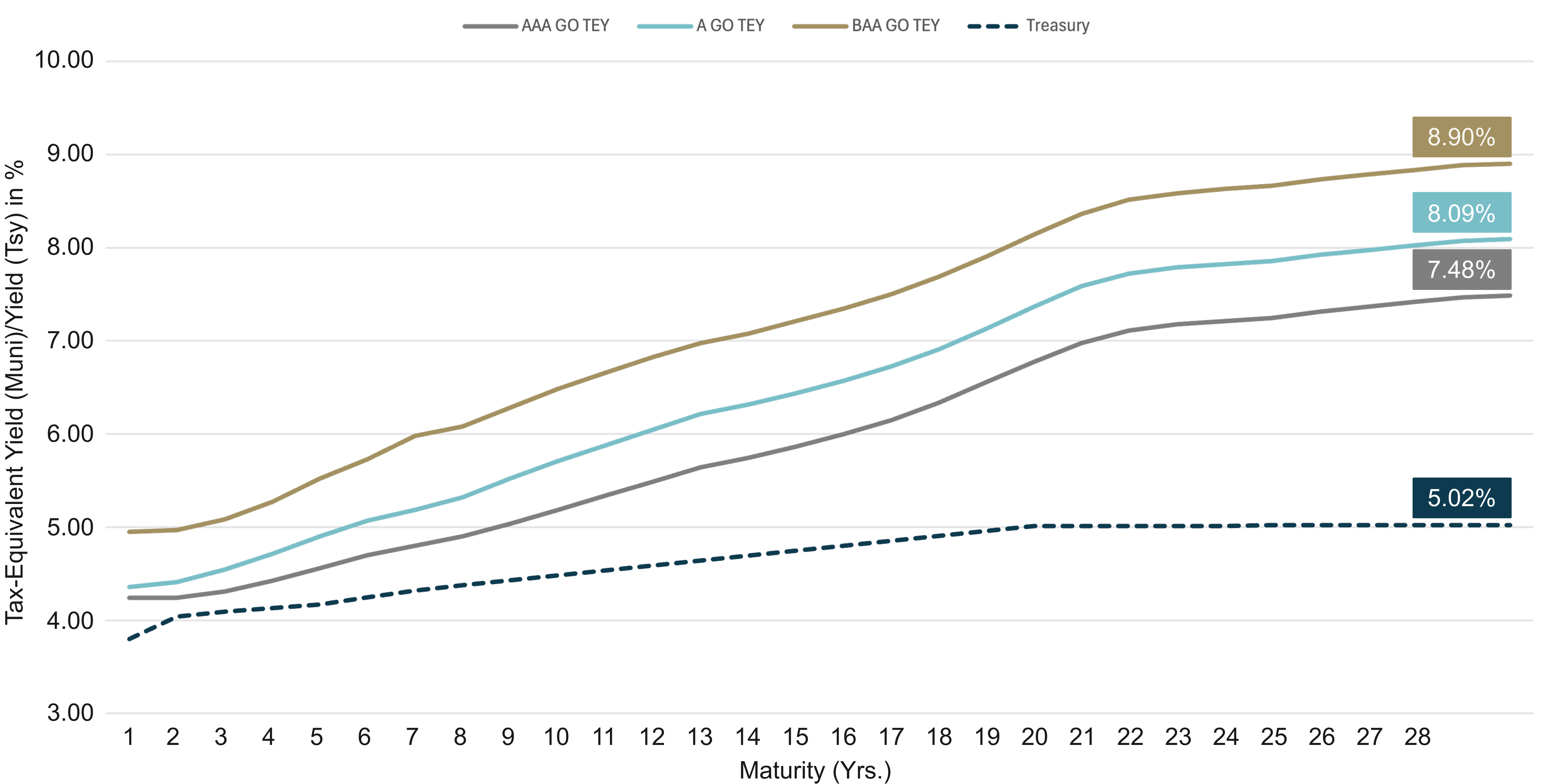

We noted in a previous commentary that, in our view, today’s environment makes for an attractive entry point into the asset class, as the market fundamentals are near the strongest levels in recent history, and yields are just off historically high levels. With the Bloomberg High Yield Municipal Bond Index yielding 5.53%, as of May 29, 2026, this brings a tax-equivalent yield of 9.34%, assuming the top U.S. tax rate of 40.8%. In other words, an investor locking in today’s attractive yields on lower-rated municipal bonds has the opportunity to position their portfolio to capture attractive income.

Assessing Revenue Bond Sectors

Within the revenue bond market, we continue to see attractive opportunities across several sectors benefiting from favorable supply-demand dynamics and stable operating fundamentals.

Healthcare issuance has remained elevated in 2026, creating opportunities to capture additional spread in select issuers with improving balance sheet trends and strong market positions. We also continue to find value in certain prepaid gas structures, which are generally supported by highly rated financial counterparties.

Transportation-related sectors—including airports, toll roads, and ports—remain appealing, as traffic volumes and revenue trends continue to normalize since the pandemic, and infrastructure investment needs persist.

At the same time, we remain more selective in areas tied to commercial real estate development, particularly within portions of the high yield market where long-term demand assumptions may prove overly optimistic.

Complexity and Dispersion Argue for Active Management

In our view, today’s municipal market increasingly rewards active management and disciplined security selection.

The combination of elevated issuance, fragmented market structure, and significant dispersion across sectors, structures, coupons, and credit profiles has expanded the opportunity set for experienced active managers. We believe having access to a broader inventory of new issues, including institutional offerings that may not be widely available through traditional retail distribution channels, can provide a meaningful advantage in identifying relative value opportunities.

That advantage may be particularly pronounced in the high yield municipal market. Many smaller or more specialized transactions are not broadly syndicated across the market and instead are placed with a limited group of institutional investors that possess dedicated credit research capabilities and experience underwriting more complex structures. These transactions can offer attractive incremental yield and structural protections relative to more widely distributed issues.

We also believe municipal market complexity continues to create opportunities for active managers to add value through security selection. Differences in structure, call features, liquidity characteristics, and state-specific trading dynamics can produce meaningful pricing inefficiencies, even among issuers with similar credit ratings. Often, particularly in the investment-grade range, there are wider spreads for coupon differences, rather than credit quality, which can potentially create attractive opportunities.

Summing Up

As municipal bonds enter the second half of 2026, we believe the asset class continues to offer a compelling combination of attractive income, potentially attractive total returns, resilient credit fundamentals, and supportive market technicals. Starting yields remain near the highest levels of the past decade, which historically have been an important driver of forward return potential across fixed-income markets.

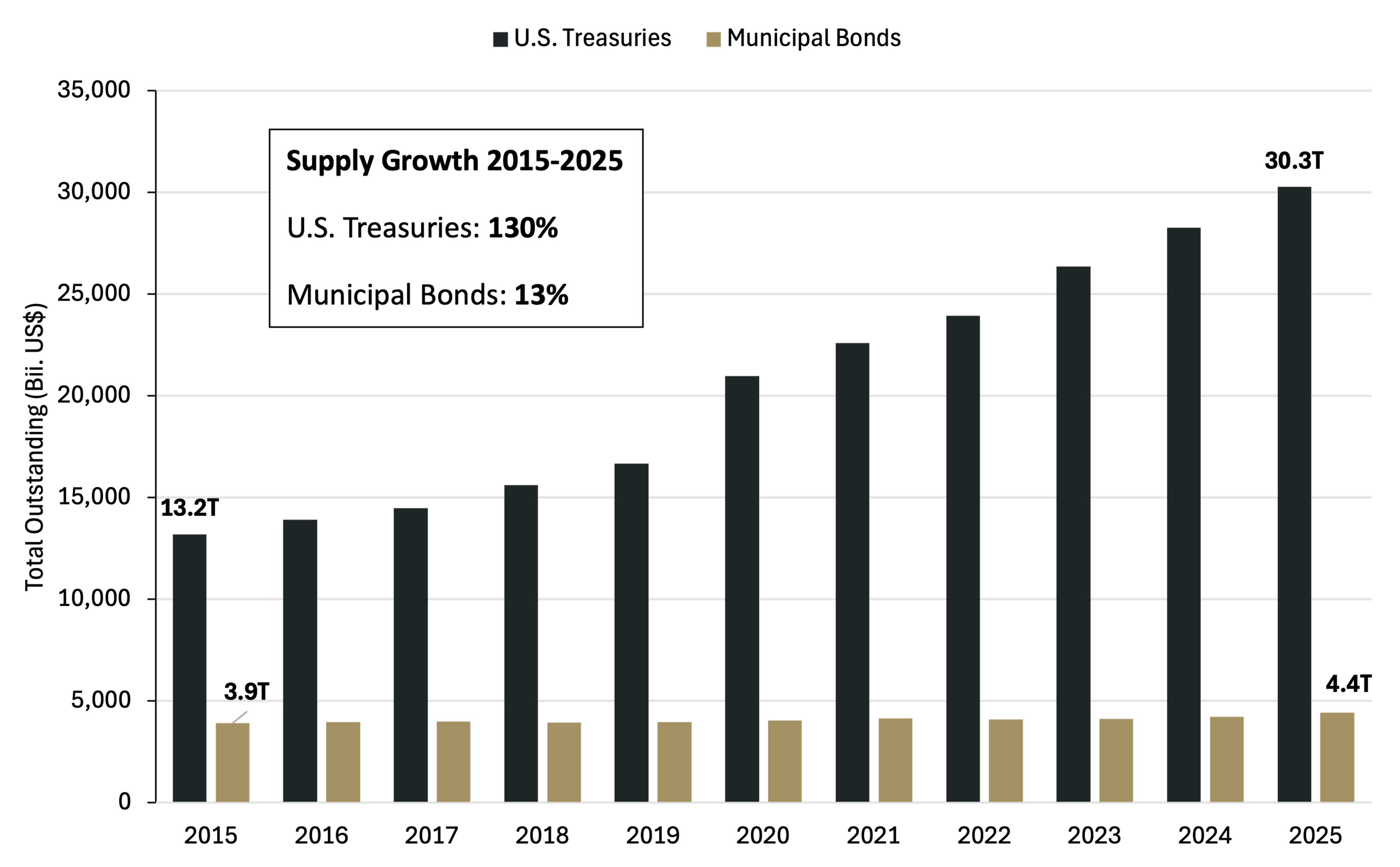

At the same time, municipal credit quality remains broadly stable, supported by healthy state and local government balance sheets, elevated reserve levels, and limited signs of broad-based credit deterioration. While issuance is likely to remain at higher levels, as municipalities continue to finance infrastructure and other long-term capital needs, investor demand has thus far remained more than sufficient to absorb the increased supply.

In our view, the shifting dynamics of today’s market environment also reinforces the importance of active management. Investors may wish to focus on experienced managers with deep credit research capabilities and broad access to both public and institutional municipal offerings.

Given these factors, we believe municipal bonds remain well positioned for investors seeking tax-advantaged income, attractive returns, and long-term portfolio diversification.