Dispersion Emerges as the Defining Theme for the Second Half of 2026

Midway through 2026, the U.S. economy remains on solid ground. While markets have absorbed geopolitical shocks and ongoing uncertainty about the impact of AI and higher oil and gas prices feeding inflationary impulses, the underlying economic backdrop remains relatively steady.

U.S. nominal gross domestic product (GDP) growth remained strong at 6% year over year in the first quarter, despite quarter-to-quarter fluctuations tied to government shutdowns. Since the end of 2025, consumer spending has remained healthy, with retail sales increasing 4.9% year over year, while the unemployment rate declined to 4.3%.

Against this supportive macroeconomic backdrop, dispersion has become the defining market theme for the second half of 2026. Normalized interest rates, AI disruption fears, geopolitical and inflation uncertainty, and shifting sector leadership have widened the gap between companies that can adapt and potentially benefit from this new regime and more vulnerable issuers that may struggle to adjust to a more demanding operating environment. Higher financing costs are reinforcing this trend, driving greater differentiation across sectors and issuers, even as higher nominal growth continues to support carry and many cyclical areas of the market. As dispersion widens, markets have become more focused on distinguishing between issuers positioned to benefit from the current environment and those more vulnerable to higher financing costs, AI disruption, or weaker operating trends.

In turn, this dispersion elevates the role of active management, where rigorous fundamental research and careful security selection are critical to seeking issuers best positioned to navigate these shifts and potentially capture differentiated sources of portfolio alpha.

Selective Positioning for AI CapEx and Elevated Carry

AI-related investments are one of the clearest examples of this dispersion and remain a key theme across both investment grade and leveraged credit markets. In high quality portfolios, the focus is on sectors that can either potentially benefit from the capital spending tied to the AI buildout or are at lower risk of disruption. These include energy, utilities, gencos (power generation companies), industrials, data centers, aerospace, and money center banks. In leveraged credit, positioning is similarly tied to the AI-driven capital expenditure (CapEx) cycle, including copper, aluminum, power infrastructure, and select AI-related issuers that continue to grow within both the investment grade and high yield markets. We avoid seeking out areas more exposed to AI-driven disruption, including certain technology and software issues.

The broader capital spending cycle has helped support earnings growth and corporate fundamentals across many cyclical and capital-intensive sectors. In our view, that remains constructive for credit, but it also requires careful issuer selection as AI disruption, higher financing costs, and shifting sector leadership continue to create potential winners and losers. We also remain cautious on consumer-related cyclicals due to elevated price pressures.

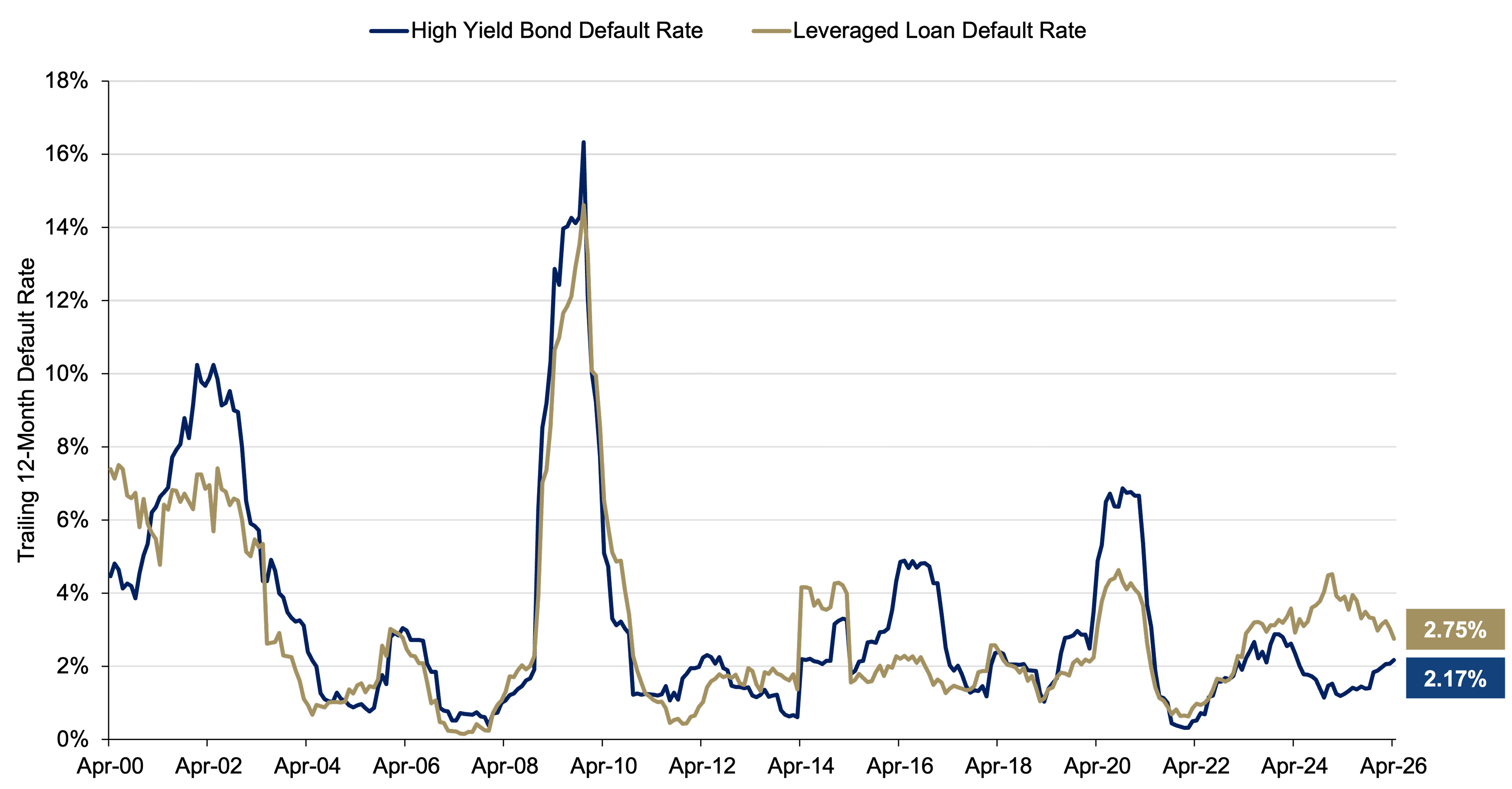

In leveraged credit, carry remains attractive while spreads remain near historically tight levels, which limits the case for broad beta exposure. Defaults across high yield bonds and leveraged loans remain relatively low by historical standards, and we continue to closely monitor refinancing needs and the impact of higher rates across more leveraged issuers.