With interest rates closer to historical norms and capital once again carrying a real price, the current environment has restored differentiation between companies with durable cash flows and those dependent on easy financial conditions. Here, we explore the importance of quality equities and the metrics active managers use to help identify opportunities in the space.

Why has quality become so important for value stocks in a higher-rate world?

When rates were near zero, the penalty for poor capital allocation decisions was much lower, and the performance gap between companies that made money and those that didn’t narrowed as valuations expanded across the market.

With interest rates at today’s levels, companies must earn well above their cost of capital to create a cushion that allows them to reinvest in their businesses or return capital to shareholders through buybacks. When rates were near zero, the distinction between companies that made money or not had much less impact on stock performance. Since rates began rising in 2021, however, the performance gap between profitable and unprofitable companies has widened significantly, creating potential opportunities for active investors to distinguish between the two with a focus on quality and discipline.

How does the growth of AI fit into a value investing framework?

Investor concerns around AI have increasingly focused on which industries and sectors could be disrupted by its adoption. The bigger source of confusion, however, is identifying who ultimately benefits. The value team views it through the same top‑down framework applied to other structural shifts across industries, whether they unfold at a micro or macro level. Within that framework, companies can be categorized into four groups:

- Companies that both we and the market believe will benefit from AI. These businesses are typically fairly valued or even expensive, reflecting broad consensus around their upside.

- Companies the market expects to benefit from AI, but where we disagree. These are companies we avoid, as we do not see the anticipated gains materializing.

- Companies that both we and the market believe will be negatively impacted by AI. These are generally uninteresting from an investment standpoint.

- Companies the market believes will be harmed by AI, but we see opportunity. This is where we are spending the most time today, as misperceptions around AI’s impact may be creating attractive entry points.

This final group, where market expectations appear misaligned with fundamentals, is where we believe active investors have the greatest opportunity to add value.

What is a modern value equity view of valuation and risk management?

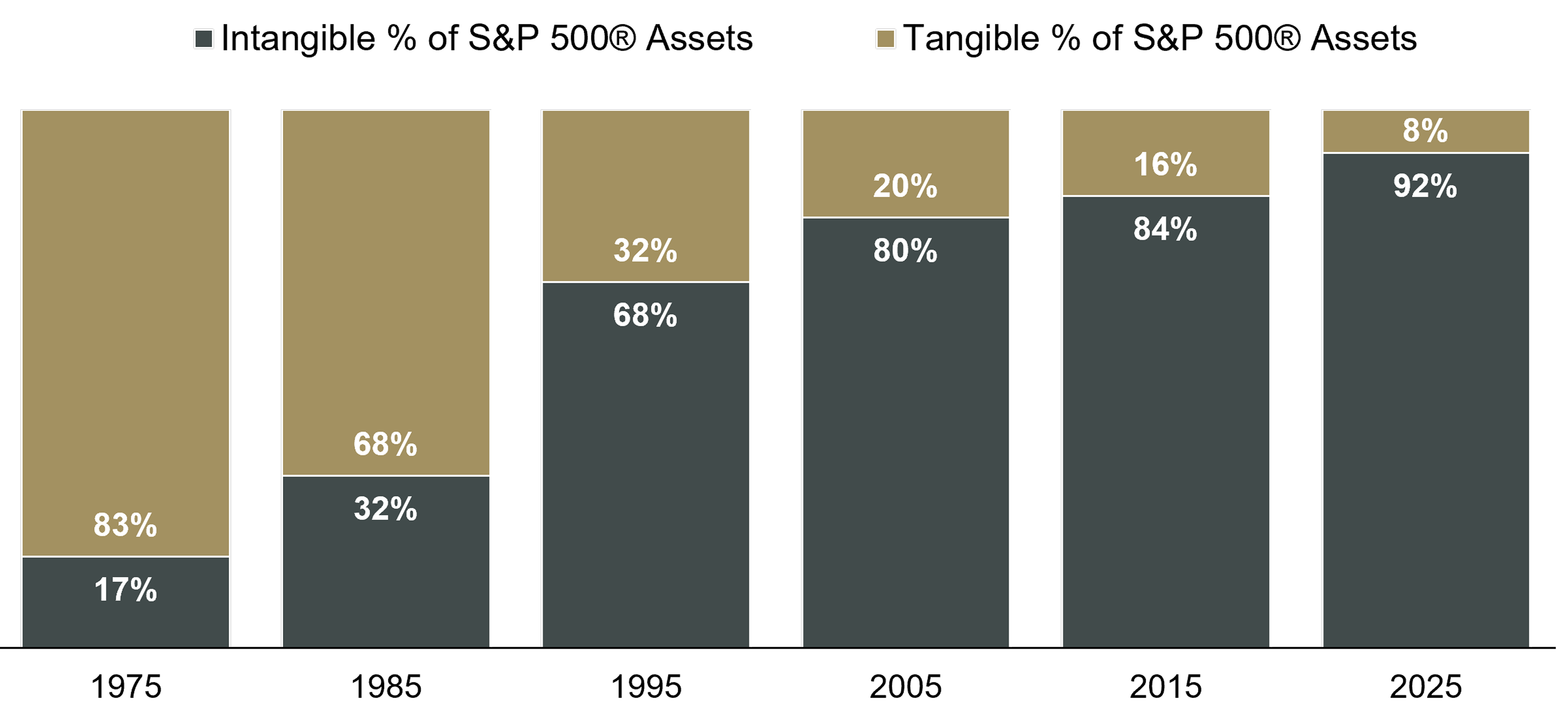

Traditional measures like price to book once defined value, but as intangible assets have become a larger driver of returns, those metrics have lost relevance (see Figure 1).