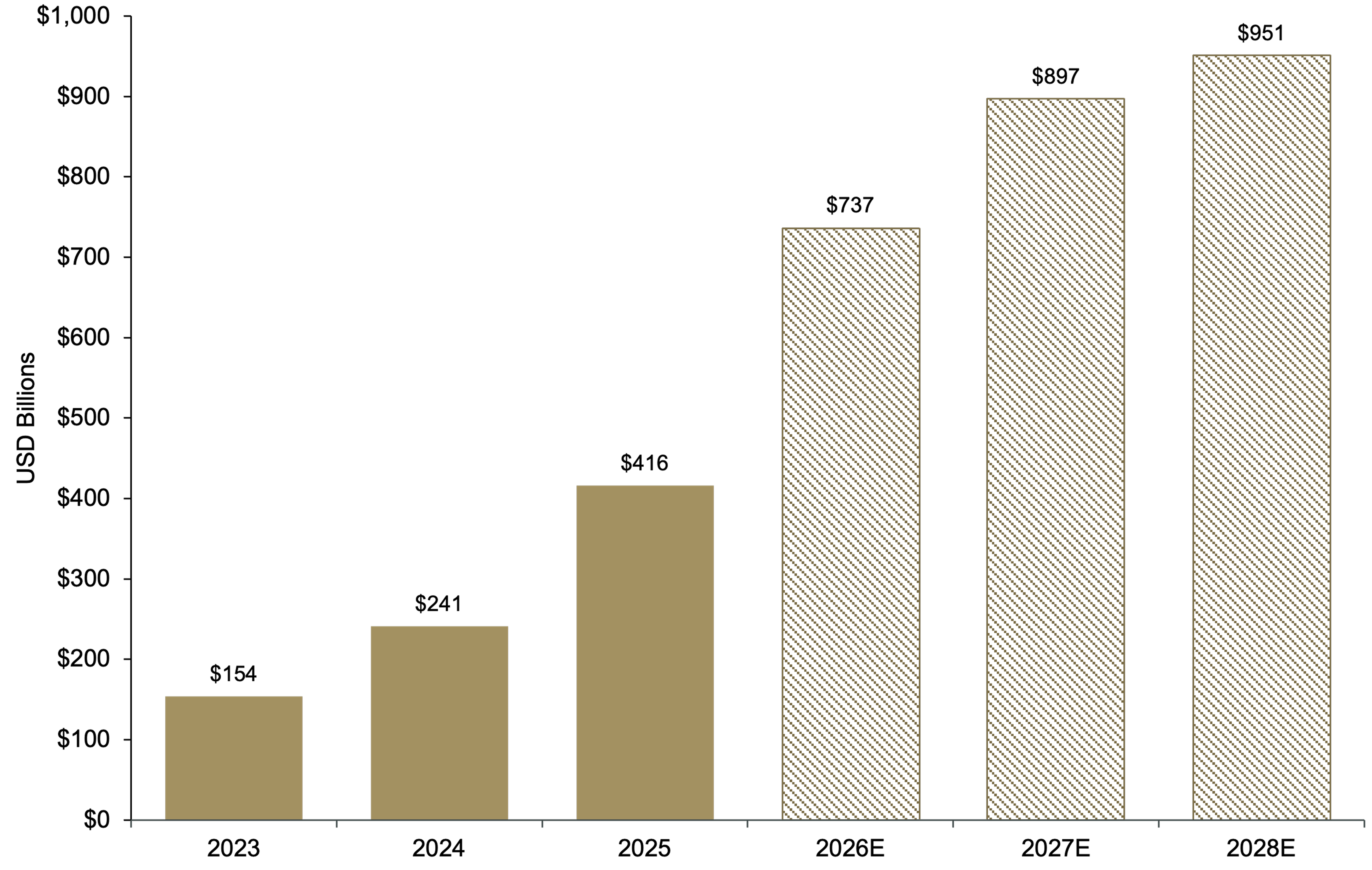

Importantly, token consumption, which is the volume of tokens processed by an AI model and a way to measure AI usage and compute demand, has grown between five times and 50 times, year over year, as of March 31, 2026. This signals a sharp inflection from training-driven demand toward large-scale inference, which is significantly more computing-intensive and persistent.

AI-driven demand has also catalyzed a broad-based recovery in semiconductor capital equipment spending. Earlier this year, a leading manufacturer announced plans to double cumulative capital expenditures over the next three years. Taken together, we expect global wafer fabrication equipment spending to reaccelerate to approximately a 20% compound annual growth rate over the next two to three years.

As the pace of AI adoption quickens, and its influence spreads across industries, one thing is certain: For many companies that believe their businesses rest on firm foundations, today’s “sure thing” may be tomorrow’s “wait, what just happened?” This creates a level of risk and opportunity for active investors, as the market tries to figure out which companies’ business models are best positioned to benefit from the adoption of AI, and which are most at risk.

As the cost and speed of advanced computing evolve, the market has questioned both the near-term momentum and terminal value of “asset-light” entities. Case in point: the software industry. For the last three decades, software companies were considered some of the best businesses in the world. High levels of recurring revenues, consistent growth, and best-in-class margins were hallmarks of the industry. That paradigm has changed with the advent of generative AI; business models that were once “eating the world,” in Marc Andreessen’s famous formulation, are now in question. Now, software is in the eye of the storm. Fears around displacement of large, established players by competitors harnessing AI’s power to rapidly and effectively generate advanced software offerings permeate the market, putting industry stocks under considerable pressure.

How are these themes playing out across our actively managed investment capabilities?

Innovation: In times of volatility, it is often helpful to take a step back and look at the bigger picture. Every technological change brings disruption. And in disruption, there is risk and opportunity. Our view of this cycle is no different. We have been cautious in our approach to the software industry for an extended period as we await further clarity. In our view, there are many traditional packaged software companies that are at severe risk of agentic AI disruption. However, others have advantages that can help insulate them from disruption and even benefit them further. Specifically, we are focused on companies with differentiated business models that are vertically integrated across several platforms, possess scale advantages, and are continuously improving internal AI tools using real-time, proprietary, "closed loop" data.

We continue to focus on the AI-led infrastructure buildout (mainly expressed through industrials and semiconductors) along with attractive opportunities in the healthcare sector, where many companies are beginning to benefit from AI-driven gains in productivity and scalability. These areas exhibit some of the best operating and technical momentum in the market.

Value: As value investors, we believe this kind of environment can be a great opportunity, helping us identify businesses we believe have durability and long-term staying power but are being penalized over the near term as investors sell the good with the bad until the dust settles. While we favor some major names that are unquestionable AI-growth driven leaders, we manage the risk and have sought out candidates whose business models have come under question by investors and the financial media, given our careful assessment of the likely AI impact. Finding these opportunities is not easy, but this is where a consistent and repeatable process, grounded in rigorous fundamental analysis, should help drive long-term outperformance.

Global & International: Here, we are favoring the companies that provide the foundations of the AI revolution. This includes foundries that supply critical chips for all major hyperscalers and AI platform providers. The surge in AI-driven demand is also catalyzing a broad-based recovery in semiconductor capital equipment spending. At the same time, memory suppliers are preparing for a synchronized upcycle across both dynamic random-access memory (DRAM) and NAND (flash memory) as well.

Long-Term Themes: Geopolitics Remains a Top Concern

The market has had to contend with Increased geopolitical uncertainty for a number of years, and those conditions are likely to continue. Russia’s invasion of Ukraine in 2022, Hamas’ attack on Israel in 2023, and most recently, the onset of the U.S.-Iran war have had direct impacts on the energy sector as well as industrials, particularly defense companies that must restock munitions and adapt to evolving battle tactics (e.g., the increasing use of low-cost drones). This uncertainty does not look like it will settle anytime soon with additional risks such as U.S.-China tension over Taiwan, supply chains, and cyberattacks all representing real tail risks.

How are our investment teams thinking about this and other key long-term themes?

Innovation: The changing geopolitical landscape has forced nations to look to their own resources to prepare for current and future instability. Many are pushing through an increase in defense spending in response to global threats. For example, the U.S. has proposed a $1.5 trillion defense budget for fiscal 2027, which would mark a $500 billion (50%) increase from the levels approved for fiscal 2026. Notably, emerging segments of defense such as hypersonics, space/satellites, and drones are expected to see 5x to 10x increases in funding, signaling strong growth prospects for companies serving these areas. And this is a global trend, with few exceptions. We believe there are many publicly traded companies across the market cap spectrum that stand to benefit from this sustainable trend, and we will continue to focus on the compelling opportunities that present themselves.

Value: While uncertainty always poses a risk to overall markets and portfolios, we maintain exposure to segments of the market that stand to benefit from heightened geopolitical risk. We believe U.S. defense contractors in the large and small cap spheres are well positioned in this environment. We also favor domestic energy producers, given the likelihood of elevated energy prices in the current geopolitical landscape.

Global/International: While defense continues to be a focus here as well—including moves to diversify into new areas such as drone technology—we are also following some other long‑term, global themes we find compelling. These include emerging innovation in healthcare and pharmaceuticals; increased investment in infrastructure and rebuilding; rising global power demand; and, of course, the disruptive impact of AI. In addition to the global semiconductor manufacturing and equipment providers mentioned earlier, we favor leaders in electrification and power management, diversified energy and infrastructure companies, and large‑capitalization pharmaceutical and life sciences companies.